A Temporary Shock or Long-Term Opportunity?

Voltamp Transformers Ltd -Powering India’s Grid Expansion

Voltamp Transformers Limited is one of India’s leading transformer manufacturers, backed by over five decades of engineering expertise and industry experience. Headquartered in Vadodara, the company manufactures power and distribution transformers, dry-type and cast resin transformers, compact substations, and ring main units. It serves diverse sectors including power utilities, renewable energy, EPC infrastructure, industrials, oil & gas, and data centers. With over 80,000 transformer installations across domestic and international markets, Voltamp has established a strong reputation for quality, reliability, and execution excellence.

Why Today’s Weakness Could Become Tomorrow’s Opportunity

The recent correction in Voltamp has raised near-term concerns but the broader long-term opportunity in India’s power and infrastructure sector remains largely intact. The company is strategically positioned to benefit from key structural trends including renewable energy expansion, grid modernization, industrial electrification, data center growth, transmission capex and smart power distribution. This positions Voltamp as a potential long-term beneficiary of India’s evolving power infrastructure cycle.

Key Financial Highlights

FY26 Revenue: ₹2,154 crore - highest-ever annual revenue achieved by the company

FY26 Net Profit: ₹305 crore - reflecting healthy profitability despite near-term margin pressure

5-Year Sales CAGR: Approximately 25%, indicating strong and consistent business growth

5-Year PAT CAGR: Around 27%, showing robust earnings compounding over the long term

ROCE: Strong return profile with Return on Capital Employed of nearly 24%

ROE: Healthy Return on Equity of around 18%, supported by efficient capital allocation

Debt Position: Virtually debt-free BS, providing strong financial stability and resilience

Market Share: Estimated 15% in India’s market, reflecting strong industry positioning

Current Manufacturing Capacity: Around 13,000 MVA annually and expected to rise to nearly 20,000 MVA after the upcoming Jarod facility commissioning

The company’s strong balance sheet, conservative financial management, healthy cash flows, and minimal leverage continue to remain among its biggest long-term strengths.

Recent Developments - Record Revenue Performance

Voltamp reported its highest-ever annual revenue in FY26 at around ₹2,154 crore, reflecting continued demand strength in the transformer and power equipment sector.

Massive Capacity Expansion – A Key Growth Trigger

The upcoming Jarod facility, expected to commence operations by July 2026, could become a major long-term growth driver for Voltamp Transformers Limited. The plant is expected to add nearly 6,000 MVA capacity, increasing total capacity to around 20,000 MVA. It is also likely to strengthen execution capability, expand the company’s presence in the higher-value EHV transformer segment, and improve operating leverage, potentially supporting stronger revenue growth and earnings over the coming years.

Strong Order Book Visibility

Voltamp Transformers Limited has entered FY27 with a strong order backlog exceeding ₹1,200 crore, supported by fresh order inflows in April 2026. Demand remains healthy across utilities, renewable energy, data centers, industrial capex, and EPC infrastructure projects, providing solid medium-term revenue visibility and supporting the company’s growth outlook.

Why the Stock Corrected Recently

The recent decline in Voltamp Transformers Limited was mainly driven by weaker-than-expected Q4FY26 earnings, marked by a sharp drop in profitability and significant EBITDA margin contraction. Margins were further impacted by the execution of older fixed-price orders booked before the surge in copper, transformer oil, and CRGO steel prices.

Earnings were also affected by certain one-time provisions and accounting adjustments, including MTM losses and employee-related provisions, most of which are non-recurring in nature. Additionally, after a strong multi-year rally, the disappointing quarterly performance triggered institutional selling and profit booking, adding further pressure on the stock in the near term.

Why the Long-Term Story Still Looks Strong

India’s Power Infrastructure Cycle Is Just Beginning: India is expected to witness significant investments in renewable energy evacuation, transmission infrastructure, smart grids, rail electrification, industrial expansion, and AI-driven data center infrastructure. Since all these sectors require large-scale transformer deployment, the long-term demand outlook for transformer manufacturers remains highly favorable.

Strong Market Position: Voltamp is widely regarded as a premium-quality transformer manufacturer with a strong execution track record, disciplined bidding approach, healthy customer relationships, and a well-established industrial presence. Despite competition from larger industry players, the company’s nearly 15% market share provides it with a meaningful and well-recognized position within the Indian transformer industry.

Financial Strength: Company stands out among cyclical capital goods companies due to its strong financial profile, supported by minimal debt, healthy cash generation, robust return ratios, and a conservative management approach. This financial strength enhances the company’s resilience and provides stability even during periods of temporary earnings weakness or industry slowdowns.

Capacity Expansion Can Change Growth Trajectory: The upcoming EHV capacity expansion could significantly alter the growth trajectory of Voltamp Transformers Limited by supporting meaningful revenue growth, improving market share, enabling participation in larger utility contracts, and enhancing long-term margins through better operating leverage. If executed successfully, the FY27–FY29 period could emerge as a major growth phase for the company.

Risks & Negatives

While long-term outlook for Voltamp remains positive, certain risks also persist like volatility in copper, aluminium, CRGO steel and transformer oil prices could pressure margins, delays in commissioning the Jarod facility may impact growth expectations.

Company faces strong competition from Hitachi Energy, CG Power and Industrial Solutions Limited and ABB. In addition, the transformer industry remains cyclical and dependent on government capex and industrial demand while valuations still appear relatively premium despite the recent correction.

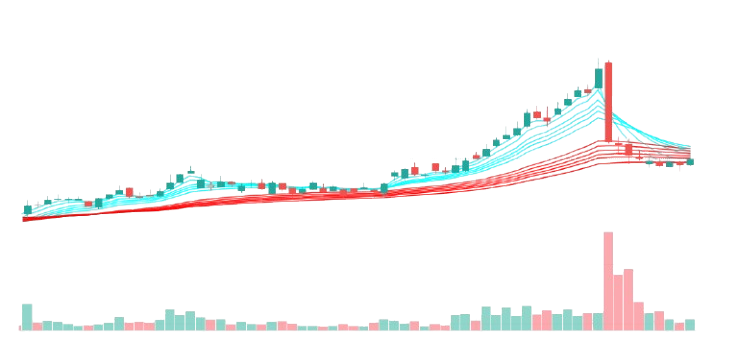

Technical Analysis — GMMA Daily Chart Reading

What the Daily Chart Suggests

The attached GMMA chart indicates:

Sharp correction after vertical rally

Short-term moving averages collapsed into long-term averages

Selling pressure appears to be cooling

Long-term trend structure still broadly intact and stock may be consolidated for long term gains

Conclusion & Investment Outlook

Voltamp Transformers continues to remain one of the fundamentally stronger companies in India’s transformer and electrical equipment sector. The recent correction appears to be driven largely by temporary factors such as margin pressure, raw material inflation, weak quarterly sentiment, and profit booking, rather than any structural deterioration in the business.

The company remains well-positioned to benefit from India’s rising power demand, grid infrastructure spending, renewable energy expansion, data center growth, and ongoing capacity expansion initiatives.

INVESTMENT VIEW

Medium Term: The outlook appears gradually improving as margins normalize, legacy low-margin contracts conclude, and the new Jarod facility enhances capacity, execution capability, and profitability.

Long Term: Backed by a debt-free balance sheet, healthy return ratios, strong execution track record, and expanding manufacturing capacity, Voltamp appears well-positioned to remain a meaningful long-term beneficiary of India’s multi-year power and infrastructure growth cycle. The recent correction could offer a favorable accumulation opportunity for medium- to long-term investors who understand cyclical businesses.

Disclaimer

This analysis is intended solely for informational purposes and does not constitute any investment or financial advice. All information is sourced from public company filings, analyst reports, and third-party sources believed to be reliable. In accordance with SEBI guidelines, market data is presented accordingly. Investors should conduct independent research, perform due diligence, and consult qualified financial advisors before making any investment decisions. The views expressed are personal and may be subject to errors or biases.

Let Us Talk

What’s your view on Voltamp’s recent correction and India’s booming transformer, renewable energy, and data center opportunity?

Is this a temporary earnings setback or a long-term accumulation opportunity? Share your investment perspective.