Bajaj at the Crossroads — Buy the Fear or Wait the Turn?

A Deep-Dive Institutional Style Report on Bajaj Finserv & Bajaj Finance

Investment Thesis Snapshot

The Bajaj financial ecosystem is currently navigating a cyclical correction amid strong underlying structural growth. While market sentiment remains weak, fundamentals across lending and insurance businesses continue to demonstrate resilience. The present phase appears to be a valuation reset rather than a structural breakdown.

Core View:

Short term: Volatile and bearish bias

Medium term: Stabilisation likely

Long term: Strong compounding opportunity

Bajaj Finserv Ltd

Bajaj Finserv acts as the holding company for the financial services arm of the Bajaj Group. It operates across multiple verticals including lending, life insurance, general insurance, and digital marketplaces.

Key Highlights:

The company operates as a diversified financial conglomerate with multiple revenue streams spanning both lending and insurance businesses. It benefits from a strong platform-based ecosystem, enabling integrated financial services delivery and cross-segment growth.

Strategic Positioning:

Acts as a “financial supermarket” benefiting from India’s financialization trend.

Bajaj Finance Ltd

Bajaj Finance is one of India’s leading NBFCs with a highly diversified lending portfolio spanning retail, SME, rural, and digital segments.

Key Highlights: The company serves a vast customer base of over 115 million, supported by strong assets under management growth of around 22–24%. It also maintains a high ROE, reflecting consistent execution and operational efficiency.

Strategic Positioning:

Core engine of credit growth for India’s middle-class consumption story.

Bajaj Finserv — Key Developments

Allianz Stake Acquisition

Acquiring 26% stake in insurance JVs (Approx ₹24,000 crore)

Full ownership expected by Oct 2026

Strategic benefit: full profit capture plus integration flexibility

Growth Metrics:

The company has demonstrated strong growth across key metrics, with AUM increasing by approx 24% and sales rising by around 25%. Despite facing macroeconomic headwinds, it has maintained stable profitability, reflecting resilience in its overall business performance.

Insurance Momentum

Strong premium collections across life & general insurance

Indicates steady underlying demand

Bajaj Finance — Key Developments

FinAI Transformation (BFL 3.0)

AI integration in underwriting, collections, onboarding

Early efficiency gains visible

Financial Performance (Q3 FY26)

In Q3 FY26, the company reported a NII growth of around 21%, although net profit was impacted due to one-time provisions. Asset quality remained stable, with net NPA at approx 0.47%. On the customer front, the company witnessed strong expansion, adding about 4.7 million customers during the quarter, taking its total customer base to around 115 million.

Risk Analysis & Technical Structure

Bajaj Finserv

Bajaj Finserv faces several key risks, including a holding company discount that may limit valuation upside and relatively high leverage of around 5x debt-to-equity. The stock has also underperformed, declining by approximately 13–14%, while potential integration risks arising from the Allianz deal could further impact its overall performance.

Bajaj Finance

Bajaj Finance faces several key risks i.e. rising asset quality concerns in the 2 & 3-wheeler segments, where gross NPAs are above 13%. There is also increasing stress in the MSME portfolio, leading to higher credit costs. Additionally, company has moderated its growth guidance to around 22–23%, while its premium valuation leaves limited room for error, making it vulnerable to any negative surprises.

Technical Analysis Summary

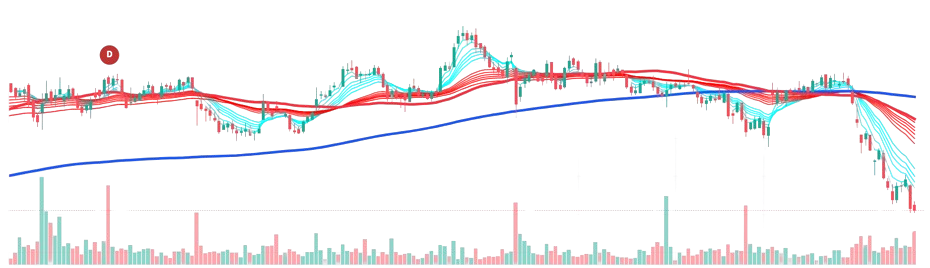

Bajaj Finserv

Bajaj Finserv is currently in a strong downtrend on the daily charts, trading below key moving averages, which indicates continued weakness in price action. The stock has important support in the 1650–1680 range, while resistance is seen between 1800 and 1900 levels. Overall, the medium-term outlook remains bearish, although the stock is approaching a significant long-term support zone that could act as a potential base.

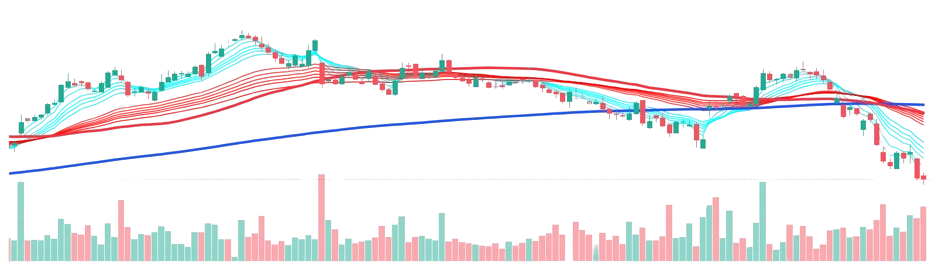

Bajaj Finance

The stock is exhibiting a clear breakdown structure, characterized by a pattern of lower highs and lower lows, indicating sustained bearish momentum. Key support is placed in the 800–820 range, while resistance lies between 880 and 920 levels. Overall, it appears weaker compared to Bajaj Finserv and will require a proper base formation before any meaningful reversal can be expected.

Growth Outlook

Bajaj Finserv is expected to remain in a consolidation phase in the near term, while the medium-term outlook is supported by benefits arising from insurance integration. Over the long term, the company stands to gain significantly from India’s low insurance penetration, positioning it well for sustained growth.

Bajaj Finance is expected to see stabilisation in asset quality in the near term, while the medium-term outlook is driven by efficiency gains from AI-led initiatives. Over the long term, the company aims to significantly expand its reach, targeting a customer base of over 200 million, which could further strengthen its growth

Valuation Perspective

Both stocks have undergone a meaningful correction, with current market pricing largely reflecting near-term risks and uncertainties. However, their long-term growth prospects remain intact and are not fundamentally impaired. The key insight is that the ongoing correction appears to be driven more by market sentiment rather than any significant deterioration in underlying business fundamentals.

Final Investment Verdict

Bajaj Finserv is recommended as an ACCUMULATE on a staggered basis, particularly attractive in the lower range of ₹1700–1850, with long-term upside expected to be driven by insurance growth and potential holding company re-rating.

Bajaj Finance, on the other hand, is viewed as a strategic BUY, offering a high-quality NBFC at a corrected valuation, with strong earnings growth visibility once normalization in asset quality and credit costs takes place.

Strategy Recommendation and Conclusion

The strategy is to avoid aggressive lump sum investments and instead adopt a staggered accumulation approach. Investors, before making choices, should also wait for technical confirmation before taking short-term trading positions.

In conclusion, the Bajaj twins represent a rare combination of scale, strong execution, and structural growth potential. Despite current market uncertainties, corrections in high-quality financial franchises like these have historically provided attractive long-term wealth creation opportunities.

Disclaimer

This analysis is intended solely for informational purposes and does not constitute any investment or financial advice. All information is sourced from public company filings, analyst reports, and third-party sources believed to be reliable. In accordance with SEBI guidelines, market data is presented accordingly. Investors should conduct independent research, perform due diligence, and consult qualified financial advisors before making any investment decisions. The views expressed are personal and may be subject to errors or bias.