Building on Resilience: Technocraft Industries Poised for Revival

A Multi-Vertical Play with Global Footprint Trading at Attractive Valuations

Technocraft Industries (India) Ltd (NSE: TIIL) is a diversified industrial enterprise with operations in drum closures, scaffolding, textiles, and engineering services. At the Current Market Price, the stock trades almost 30% below its 52-week high, offering an attractive entry point for medium- to long-term investors. The company’s market capitalization stands at ₹5,700 crore.

Recent Highlights

UK Expansion (Oct 2025): £10 million (₹104 crore) investment to scale up digital engineering operations in the UK, creating high-skilled jobs.

FY25 Financials:

Revenue: ₹2,596 crore (TTM ₹2,608 Cr); Net Profit: ₹263 crore (TTM ₹261 Cr); Operating Margin: 16%; Dividend: ₹20 per share (interim)

Fundamentals & Strengths:

The company operates across diversified verticals, reducing business concentration risk and maintaining a strong global presence with exports to over 80 countries. It has delivered a solid 10-year average ROE of 17% and enjoys high promoter confidence with 74.8% holding and no pledging. Capacity expansion at the Aurangabad facility further strengthens operations, adding 1,500 MT/month steel tube and 60,000 sqm/month formwork capacity.

Concerns:

Margins have come under pressure, with OPM falling from 20% in FY23 to 16% in FY25, while profit growth remains flat (3-year CAGR of -2%). The company’s long cash cycle of 269 days reflects high working capital needs, alongside low dividend payout (5.9%) and elevated inventory levels.

Valuation Snapshot:

Technocraft currently trades at a P/E ratio of 22x and with a book value of ₹772 per share and an EPS (TTM) of above ₹111. Based on fundamentals, the fair value is much above the CMP, indicating an 18–23% upside potential. At current levels, Technocraft remains attractively valued, trading at a 30% discount to its 52-week high, supported by consistent revenue growth and a strong balance sheet.

Growth Outlook (FY26–28E)

Revenue CAGR: 15–18%; PAT CAGR: 18–22%

Margin Recovery: OPM expected to rebound to 17–18% by FY27.

Strong order book in formwork and scaffolding backed by infrastructure demand.

Investment Thesis

Why Invest?

30% correction from peak offers a margin of safety.

UK expansion adds high-margin revenue streams.

Beneficiary of India’s infrastructure growth.

Export diversification across 80 plus countries.

Favorable technical setup indicating base formation.

Stable management and strong corporate governance.

Key Risks: Margin volatility, high working capital, export dependence, and tariff uncertainties.

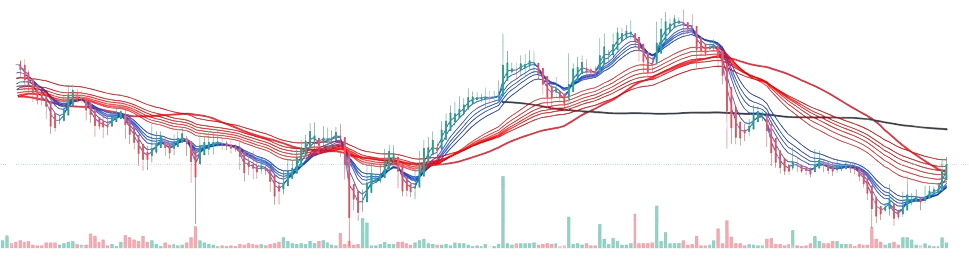

Technocraft Industries appears to be in early Stage 2, having completed its Stage 1 accumulation phase. The incoming weeks will be crucial — a sustained move above ₹2,500 with strong volumes would confirm the Stage 2 breakout, opening momentum opportunities toward much higher prices, however, failure to hold above this level could lead to further base building within Stage 1.

Fundamentally, TIIL presents a compelling long-term OPPORTUNITY backed by its diversified business model, robust operational capabilities, and expanding global footprint, which together provide healthy visibility for earnings growth. While short-term margin pressures persist, the valuation comfort and improving technical setup support a positive bias for accumulation.

Risk Level: Moderate; Investment Horizon: 18–36 Months

Disclaimer

This analysis is intended solely for educational and informational purposes and does not constitute any investment or financial advice. Past performance is not indicative of future results. All information is sourced from public company filings, analyst reports, and third-party sources believed to be reliable. In accordance with SEBI guidelines, market data is presented with a three-month lag. Investors should conduct independent research, perform due diligence, and consult qualified financial advisors before making any investment decisions. The views expressed are personal and may be subject to errors or bias.