Gayatri Projects: The ₹8,100 Crore Debt Story That Refused to Die

From Insolvency to Opportunity: Can Gayatri Become India's Next Infrastructure Turnaround Story?

Gayatri Projects has emerged as one of the most interesting special situation opportunities in the Indian stock market. Unlike conventional investments driven by earnings growth, the investment thesis here revolves around debt resolution, asset recovery, balance-sheet repair, promoter re-entry and possibility of a long-term corporate revival.

The turning point came when the Hyderabad bench of the NCLT approved a promoter-backed OTS of approx ₹2,400 crore against lender dues of nearly ₹8,100 crore. If the settlement has indeed been substantially implemented and lender obligations have been discharged - which is reported completed and the liability been closed, Gayatri may have crossed the most difficult phase of its corporate journey.

The key question for investors is no longer whether the company survives, but how much value can ultimately be unlocked from its assets, receivables, claims, and operating franchise.

The Defining Catalyst – NCLT Approved OTS

The most important development in the Gayatri Projects story is the implementation of the ₹2,400 crore OTS.

For years, the company remained trapped under excessive debt, lender pressure, funding constraints, delayed project payments, and insolvency concerns. The massive debt burden effectively overshadowed the value of its underlying assets and significantly reduced visibility for equity shareholders.

The settlement has potentially changed the narrative.

Why the OTS Matters

The debt resolution process has:

Improved the company’s survival prospects.

Reduced lender overhang.

Strengthened balance-sheet stability.

Improved clarity around asset ownership.

Created a pathway for business revival.

In many turnaround stories, the biggest gains occur after investors become convinced that survival is no longer the primary concern. Gayatri appears to be entering that phase.

Balance Sheet Transformation

One of the most encouraging developments in the turnaround story is the visible strengthening of its balance sheet. The company currently has a market capitalization of approximately ₹1,000–1,100 crore, while borrowings have reportedly reduced to around ₹311 crore. It also reports reserves of about ₹569 crore, investments of nearly ₹230 crore, and other assets exceeding ₹1,800 crore, along with fixed assets and capital work-in-progress.

The sharp reduction in debt is arguably the most important financial development for shareholders. The value of the company’s assets was overshadowed by lender claims and financial stress. However, with the debt resolution process, the market may increasingly focus on the company’s underlying assets, receivables, investments, and recovery potential rather than its historical liabilities. This transition from a creditor-dominated balance sheet to one where asset value can potentially accrue to equity holders is often where significant value creation begins in special situation investments.

Asset-Based Valuation: Looking Beyond Earnings

Traditional valuation metrics may not fully capture Gayatri’s current opportunity.

The more relevant question is that What remains after debt resolution?

Gayatri continues to own a sizeable asset base comprising:

Trade receivables

Investments

Loans and advances

Cash balances

Infrastructure SPVs

Subsidiary interests

Land parcels

Offices and project facilities

Other operating assets

The reported asset base remains substantially higher than the company’s current market capitalization. This suggests the market may still be discounting historical distress rather than potential post-restructuring value. The real issue is not asset existence but asset recoverability.

Trade Receivables: A Potential Hidden Goldmine

One of the most overlooked aspects of the Gayatri story is its receivables and claims portfolio. These balances may include:

Certified project bills

Government receivables

Contractual claims

Arbitration awards

Retention money

Even a partial recovery of these outstanding receivables could significantly strengthen the company’s financial position. For a business with a market capitalization of around ₹1,000 crore, successful realization of a meaningful portion of these dues has the potential to act as one of the most significant value-unlocking catalysts over the next few years, enhancing both balance sheet strength and shareholder value.

Loans, Advances & Legacy Claims

Infrastructure companies often hold significant value in recoverable advances, security deposits, contractual claims, and arbitration receivables. With debt restructuring largely behind it, management can now focus on recovering and monetizing these assets. At the current valuation, even modest recoveries could meaningfully enhance shareholder value.

Immovable Assets: The Underappreciated Opportunity

A significant part of the Gayatri story lies in its asset base.

Over decades of infrastructure development, the company accumulated interests in:

Land parcels

Corporate offices

Equipment yards

Project facilities

Road project SPVs

Subsidiary-owned assets

Infrastructure concessions

Historically, these assets attracted little attention because lender claims overshadowed their value. If encumbrances have been substantially removed through the OTS process, investors may gradually begin reassessing the underlying worth of these assets.

Promoter Re-Entry: A Potentially Powerful Signal

The most interesting development is the sharp increase in promoter participation. Older disclosures showed promoter ownership near 4%, whereas recent disclosures indicate promoter-group ownership of approximately 23.13%, with Tikkavarapu Venkata Sandeep Kumar Reddy alone holding around 21.5%.

For special situation investors, this development deserves close attention.

Why It Matters

Promoters typically have the best visibility on:

Settlement implementation

Asset recoveries

Receivable collections

Arbitration outcomes

Business revival opportunities

Strategic initiatives

A substantial increase in promoter ownership often signals:

Confidence in future value creation

Control consolidation

Alignment with minority shareholders

Belief in a successful turnaround

Who is T. V. Sandeep Kumar Reddy?

Tikkavarapu Venkata Sandeep Kumar Reddy is the Chairman and Managing Director of Gayatri Projects and is widely regarded as the architect of the Gayatri Group’s expansion into infrastructure, roads, power, renewable energy, real estate, hospitality, and bio-organics.

He holds:

B.S. in Civil Engineering from Purdue University

M.S. in Construction Engineering & Management from the University of Michigan, Ann Arbor

With more than three decades of industry experience, his increased ownership may indicate renewed confidence in the future of the listed entity.

For investors, the critical question is whether management can successfully convert receivables, claims, investments, and infrastructure assets into sustainable shareholder value over the next few years.

Cash Flow: The Next Phase of the Story

Historically, Gayatri’s biggest challenge was liquidity rather than asset ownership.

The company struggled with:

Excessive debt

Working capital stress

Delayed customer payments

Limited access to funding

Going forward, cash generation could be supported by:

Revival of EPC execution

Recovery of receivables

Arbitration settlements

Asset monetization

Sale of investments

Release of working capital

If management succeeds in converting balance-sheet assets into cash, the turnaround story could gain significant momentum.

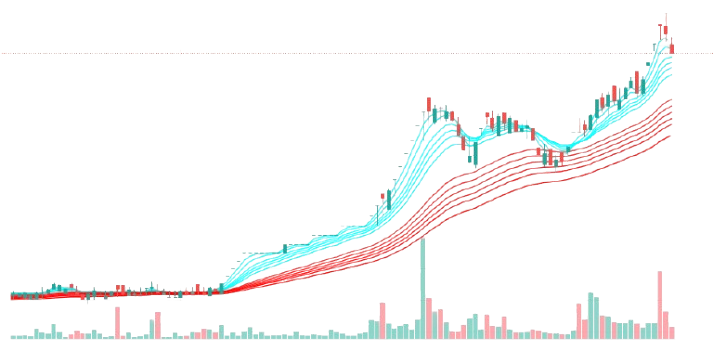

Technical Perspective

The stock’s technical structure has improved significantly over recent months.

Positive Signals

Strong long-term uptrend

Bullish GMMA alignment

Rising volumes

Signs of accumulation

Trading above key moving averages

The recent correction appears more consistent with profit booking after a strong rally rather than a complete trend reversal.

Key Levels

Near-term support: ₹22–23

Major support zone: ₹20–21

As long as these levels hold, the broader technical structure remains constructive.

Future Scenarios

Bull Case

Gayatri after successfully completing the OTS process, if recovers significant receivables, unlocks asset value, revives EPC operations, and continues to witness promoter accumulation, the market could begin valuing it as a turnaround infrastructure company rather than a distressed asset. Under such a scenario, a market capitalization of ₹2,500–5,000 crore over the longer term cannot be ruled out.

Base Case

If debt concerns continue to fade, receivables are gradually recovered, operations stabilize, and investor confidence improves, the company could continue its re-rating journey and create meaningful value for shareholder over the medium term.

Bear Case

The risks remain substantial. Asset recoveries may disappoint, receivables could prove difficult to collect, new project inflows may remain weak, legal disputes may persist, and cash generation could remain inadequate. Under such circumstances, the stock may continue to trade as a highly speculative and volatile investment.

Final Assessment

Gayatri Projects today exhibits many of the characteristics that deep-value and turnaround investors actively seek:

✔ Completion of NCLT-approved debt resolution

✔ Significant reduction in borrowings

✔ Potential asset value exceeding market capitalization

✔ Large receivable recovery optionality

✔ Infrastructure sector tailwinds

✔ Increased promoter participation

✔ Emergence of influential shareholders

✔ Strong technical accumulation pattern

The central investment question is no longer whether the company survives BUT is How much of Gayatri’s assets, receivables, claims, investments, and infrastructure franchise can ultimately be converted into value for equity shareholders?

With the ₹2,400 crore settlement, Gayatri Projects may have already crossed the most difficult phase of its corporate life cycle. Whether it evolves into a genuine multi-year turnaround story will depend on execution, asset recovery, capital allocation discipline, and management’s ability to rebuild a sustainable operating business.

This is not a conventional investment but a classic special situation where uncertainty remains high. For patient investors capable of enduring volatility and operational risks, Gayatri Projects may offer the potential for substantial value creation if the turnaround thesis plays out successfully.

Disclaimer

This report is prepared solely for educational, informational and discussion purposes and should not be construed as investment advice, a recommendation, or a solicitation to buy or sell securities. The analysis is based on publicly available information, financial disclosures, market data, and investor interpretations available as of June 2026. Certain assumptions regarding asset recoveries, promoter actions, debt resolution and future business prospects may not materialize. Special situation investments involve significant risks, including capital loss, illiquidity, regulatory uncertainties, and execution failures. Investors should conduct their own independent research, consult qualified financial advisors, and carefully assess their risk tolerance before making any investment decisions.