Kaynes Technology India: Sky-High Valuations Meet Execution Reality

Are Stellar Growth Expectations Justifying this Premium Pricing, or Is Reality About to Bite?

Executive Summary

Kaynes Technology India presents a classic high-growth, high-valuation dilemma. Trading around ₹5,700 with a staggering P/E of 130x, this electronics manufacturing services provider has delivered impressive 51% revenue growth in FY25 to ₹2,722 crore, backed by a robust ₹6,597 crore order book. However, concerning technical patterns, execution hiccups, and negative operating cash flows of ₹82 crore despite strong profits raise serious questions about sustainability at current valuations.

Company Overview & Strategic Position

Established in 1988, Kaynes has evolved into India's leading integrated electronics manufacturing services provider, specializing in automotive, aerospace, defence, medical, and space sectors. The company has strategically expanded into semiconductor assembly and high-density PCBs, positioning itself as a key beneficiary of India's electronics manufacturing boom under PLI schemes.

Recent strategic moves include acquiring Fujitsu's power module business for ₹85 crore, incorporating Kaynes Space Technology for satellite manufacturing, and ISRO partnerships.

Financial Snapshot

Strong Growth Metrics:

Revenue CAGR: 49% over 5 years (₹368 crore to ₹2,722 crore)

FY25 Performance: 51% revenue growth, 15.1% EBITDA margin (up 101 bps)

Profitability: Net profit ₹294 crore (60% growth), ROE 19.4%, ROCE 19.2%

Order Book: ₹6,597 crore with 18–24-month execution timeline

Concerning Trends:

Operating Cash Flow: Negative ₹82 crore in FY25 despite strong profits

Working Capital: 87 days, indicating significant capital intensity

Free Cash Flow: Consistently negative due to aggressive expansion

Debt Metrics: Manageable at 0.17 D/E ratio with ₹1,100 crore cash reserves

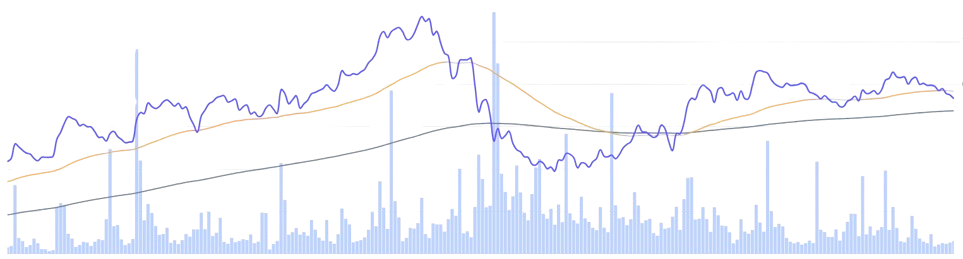

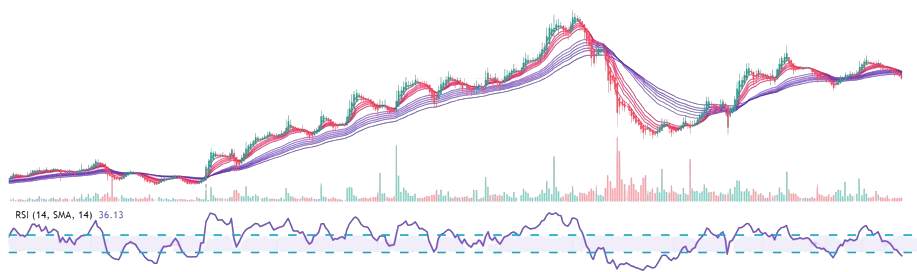

Technical Analysis

The stock has corrected 40% from November 2024 highs of ₹7,800 to February lows of ₹4,600, currently consolidating around ₹5,700. RSI at 36 approaches oversold territory, suggesting potential bounce opportunities, though lower highs indicate weakening momentum.

Growth Outlook & Execution Challenges

Management targets over 60% FY26 revenue growth with margins expanding to 15-16%. The company aims for ₹1 billion revenue by FY28, driven by aerospace, automotive, and space orders. Export revenue is targeted at 15% in FY26, expanding to 20-25% medium-term, leveraging China+1 opportunities.

However, execution challenges emerged with ₹100 crore orders incomplete in Q3 FY25, leading to 19% stock decline. Employee costs surged from ₹24 crore to ₹58 crore year-on-year, impacting margins. The Deputy CFO's resignation and ongoing SEBI scrutiny add near-term uncertainties.

Shareholding Dynamics

Institutional sentiment shows mixed signals. Promoter holdings declined from 57.83% to 53.52%, while FIIs reduced stakes from 14.84% to 10.71%, possibly reflecting valuation concerns. Conversely, domestic institutions increased holdings from 15.04% to 22.40%, with mutual funds raising stakes from 12.84% to 18.91%, indicating growing domestic confidence despite foreign caution.

Investment Strategy

Given the complex risk-reward profile, a cautious phased approach appears prudent:

Conservative Approach: Wait for RSI 25-30 levels, to time the entry and Risk Rewards

Aggressive Approach: May start 20-25% position at current levels, average down if further corrected

Long-term Investors: Current levels reasonable for 2–3-year horizon with strict position sizing

Recommended Phases:

Phase 1: 20-25% at current price

Phase 2: 35% if RSI hits 25-30

Phase 3: 40% if prices correct by 10% to 16% on broader market weakness

Final Verdict: CAUTIOUS BUY 🟡

Kaynes represents a high-quality business in a structurally growing sector with strong order visibility and government support. The 40% correction has likely discounted many operational concerns, making current levels more reasonable than peak valuations. However, extreme P/E multiples, execution challenges, and negative cash flows demand careful position sizing and risk management.

Rating Rationale:

Technical oversold conditions offer better entry opportunity

Major correction has absorbed negative sentiment

Strong order book provides 18–24-month revenue visibility

Disclaimer

This analysis is for educational purposes only and does not constitute investment advice. Past performance is not indicative of future results, and all investments carry substantial risk of loss. The information is based on publicly available data and may contain errors. Market conditions can change rapidly, affecting stock performance. Readers should conduct independent research and consult qualified financial advisors before making investment decisions. The authors may or may not hold positions in mentioned securities and are not responsible for any losses incurred.

Let Us Talk

What's your take on Kaynes' current valuation versus execution challenges? Share your thoughts on whether this premium pricing is justified given the technical setup and fundamental concerns we've highlighted!