Lokesh Machines Ltd: An Engineering Turnaround Gathering Momentum

Precision Manufacturing, Smart Capital Allocation, and the Entry of a Marquee Investor Could Shape the Next Growth Phase

Lokesh Machines has steadily evolved from a traditional machine-tool manufacturer into a niche precision engineering company with exposure to CNC machines, aerospace, defence, and automotive manufacturing. After several subdued years, FY26 appears to mark the beginning of an operational turnaround, supported by improving profitability, stronger order inflows, and renewed investor interest.

Adding to the positive sentiment is the recent preferential allotment, which saw Zenila Ventures LLP, an investment vehicle associated with the Patel family of Zydus Lifesciences, acquire a stake in the company. While this alone is not an investment thesis, it reflects growing confidence in Lokesh Machines’ long-term growth potential.

Company Profile

Lokesh Machines is a well-established Indian precision engineering and machine-tool manufacturer, specializing in CNC Turning Centres, Special Purpose Machines, precision automotive components, cylinder heads and engine blocks, and high-value machining solutions for the aerospace, defence, and industrial sectors. Operating from its manufacturing facilities in Hyderabad, the company serves both domestic and export markets. Its expertise in specialised precision machining, where long customer qualification cycles and technical know-how create high entry barriers, has helped it build lasting relationships with OEMs and industrial customers while strengthening its presence in niche engineering segments.

Business Position & Market Opportunity

While Lokesh Machines may not match the scale of industry leaders BUT has established a strong niche in precision engineering by serving automotive OEMs, defence, aerospace, heavy engineering, and industrial automation. Its technical expertise, customised machining solutions, and long-standing customer relationships position it well in specialised segments where quality and engineering capabilities are key differentiators.

The company also stands to benefit from powerful long-term industry tailwinds, including Make in India, defence indigenisation, PLI schemes, rising private sector capex, and the global China+1 sourcing strategy. Together, these trends are expected to drive sustained demand for advanced machine tools and precision engineering solutions, creating a favourable growth environment for Lokesh Machines over the coming years.

Recent Developments

Several developments have significantly improved investor sentiment:

FY26 reported a sharp improvement in quarterly profitability and revenue compared with the previous year.

The company completed a preferential issue of 13 lakh equity shares to non-promoter investors at ₹181.71 per share.

The company was removed from the U.S. OFAC sanctions list, potentially restoring smoother access to international customers and financial transactions.

Collectively, these events have materially improved the company’s perception among investors.

Zenila Ventures LLP – Why the Market Is Watching

One of the most significant recent developments for Lokesh Machines is the entry of Zenila Ventures LLP through a preferential allotment. The investment firm invested approximately ₹10.90 crore, acquiring a 2.80% non-promoter stake in the company. Given Zenila Ventures’ association with the Patel family of Zydus Lifesciences and its focus on long-term value investing, its participation lends additional credibility to Lokesh Machines’ growth story. While this should not be viewed as the sole investment thesis, it reflects growing confidence in the company’s long-term potential.

Why is this important?

Zenila Ventures appears to function as a family investment office associated with Pankaj Ramanbhai Patel, belonging to the promoter family of Zydus Lifesciences.

Zenila Ventures LLP follows a selective, long-term investment approach, focusing on manufacturing, engineering, healthcare, logistics, financial services, and consumer businesses. Its preference for fundamentally strong businesses with scalable growth potential has made its investments worth tracking among long-term investors. The LLP generally prefers minority investments rather than acquiring control.

Investment Thesis

The market generally tracks such investors because:

They usually conduct extensive due diligence.

They tend to invest with a multi-year horizon.

They prefer businesses where operational improvements can unlock value.

However, investors should avoid treating the entry of a marquee investor as a standalone investment thesis. The long-term outcome will still depend on Lokesh Machines’ execution, profitability and cash-flow generation.

Financial & Fundamental View

Positives

Improving revenue trend

Return to profitability

Healthy manufacturing opportunity

Precision engineering niche

Strong operating leverage if capacity utilisation improves

Areas to Watch

Historically modest ROE and ROCE

Working-capital intensity

Higher receivable days

Cyclical order inflows

Limited dividend history

Valuation

Historically, Lokesh Machines traded at depressed valuations because of:

inconsistent earnings,

cyclicality,

weak return ratios.

If management sustains earnings growth over the next few years, the market may increasingly value it as a niche engineering company rather than a cyclical machine-tool manufacturer.

The recent rerating suggests investors are beginning to price in that possibility, but sustained execution will be essential to justify higher valuations.

Key Positives for Long-Term Investors

✓ Engineering business with high entry barriers

✓ Manufacturing-focused India theme

✓ Defence & aerospace opportunity

✓ Precision machining capability

✓ Improving profitability

✓ Strong technical breakout

✓ Potential operating leverage

Risks

Engineering remains a cyclical sector.

Large order delays can affect quarterly earnings.

Working-capital requirements remain elevated.

Export demand may fluctuate.

The recent rally could lead to periods of consolidation after sharp gains.

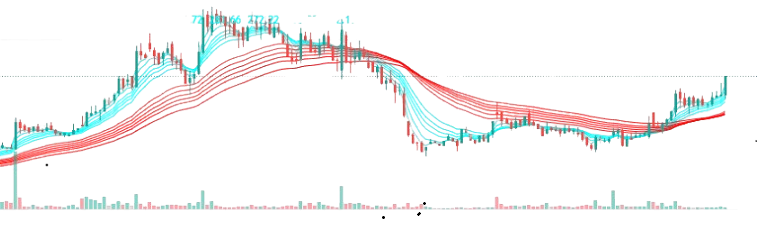

Technical Analysis

Based on the attached weekly chart:

Trend

The stock has completed a long multi-year base formation and recently broken out above previous resistance with expanding volumes.

GMMA

All moving averages are positively aligned. The price is trading comfortably above the entire GMMA ribbon, indicating a strong primary trend.

RSI

RSI around 72 indicates strong momentum. While this is in the overbought zone, stocks in strong uptrends can remain overbought for extended periods.

Medium-Term Outlook

Primary trend remains bullish.

Pullbacks toward the GMMA ribbon may offer healthier entry opportunities.

Momentum remains firmly with buyers.

Long-Term Outlook

If execution continues and earnings improve consistently, the chart suggests the possibility of a sustained structural uptrend rather than merely a short-term rally. Investors should nevertheless expect intermittent corrections after sharp advances.

Conclusion

Lokesh Machines appears to be entering a more promising phase than it has seen in several years. The combination of improving operating performance, exposure to India’s manufacturing cycle, fresh capital infusion, and the participation of a respected long-term investor such as Zenila Ventures LLP has strengthened the investment narrative.

That said, the company is still in the early stages of its turnaround. Investors should focus on whether management can consistently improve return ratios, cash flows, and order execution over the coming years. If those metrics continue to improve, the recent market re-rating could prove to be the beginning of a longer-term value creation story rather than a one-off rally.

Final Take

For investors comfortable with small-cap engineering businesses and their inherent cyclicality, Lokesh Machines deserves a place on the watchlist. Existing shareholders may continue to monitor execution and use periodic corrections to evaluate accumulation, while new investors should balance the improved outlook with prudent position sizing after the recent sharp price move.

Disclaimer

This report is intended solely for educational and informational purposes and should not be construed as investment advice or a recommendation to buy or sell any security. Investors should conduct their own due diligence, review the company’s latest financial disclosures, and consult a qualified financial adviser before making investment decisions.

Let’s Talk

What are your views on Lokesh Machines and its long-term prospects?

Does the entry of Zenila Ventures LLP signal the beginning of a long-term re-rating for the company?

Can Lokesh Machines emerge as a meaningful beneficiary of India’s manufacturing, defence, and precision engineering growth story?

What key opportunities or risks do you believe investors should keep an eye on over the next few years?

I’d love to hear your perspective—share your thoughts in the comments and let’s discuss!

New one... added to watchlist n syllabus (for study)...🙂