Medi Assist Healthcare Services Ltd

“Heartbeat of Health InsureTech” – Riding India’s Health Insurance Digitization Wave

Medi Assist Healthcare Services Ltd is India’s leading health-tech and Third-Party Administrator (TPA) for insurers, corporates, and government health schemes. With a network of 18,000+ hospitals across 1,000+ cities, it delivers claims processing, hospital network management, analytics, and digital health-benefit services through its subsidiaries like MedVantage, Raksha TPA, and Paramount TPA.

Recent Developments:

9M FY25 revenue up 14% YoY, PAT up 54% YoY.

CARE AA- (Stable) rating reaffirmed (Mar 2025).

Bessemer India Capital exited 15.7% stake in Aug 2025 (₹577 crore).

Star Health partnered with Medi Assist to outsource claims via its AI platform and Lock-in share expiry in Jul 2025 led to temporary supply-side pressure.

Financial Snapshot (FY25 estimates):

Market Cap: ₹4,200–4,300 crore | P/E: 44× |

ROE/ROCE: ~17–19% | Book Value: ₹75–80 | Net Debt: NIL

Asset-light model with steady double-digit revenue growth and strong cash flows.

Growth Drivers:

Expanding Indian health-insurance penetration and outsourcing of claims.

Consolidation among TPAs gives scale advantage to Medi Assist.

Rising share of retail and AI-driven digital processing.

Low leverage, high ROE, and technology-led cost efficiency.

Risks: Fee yield compression, insurer in-house claims processing, and share-supply overhang.

Valuation & Outlook:

At around ₹565 (P/E 44×), Medi Assist trades at a premium valuation — yet this premium appears well-earned given its strong fundamentals, scalable business model, and consistent profit growth. The company’s asset-light structure, robust ROE profile, and rising digital adoption in health-insurance administration support long-term value creation. Earnings visibility remains high, with healthy double-digit growth potential driven by technology integration, expanding client base, and margin resilience.

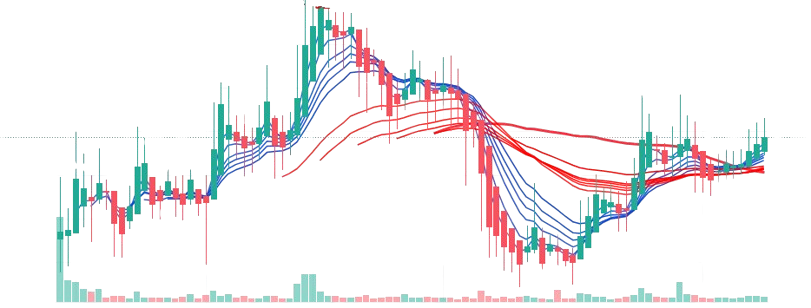

Technical View:

The stock has turned technically positive, trading firmly above its 200-day moving average with strengthening GMMA ribbons signaling renewed medium-term momentum. An RSI near 64 reflects sustained buying interest without signs of overextension. The overall setup indicates the formation of a Stage 2 uptrend following a prolonged consolidation phase — suggesting continued accumulation bias.

Recommendation:

Medi Assist Healthcare Services Ltd merits for investors seeking steady compounding exposure in India’s fast-growing health-insuretech ecosystem. The company’s structural tailwinds, financial discipline, and expanding digital moat make it a quality long-term portfolio candidate.

Disclaimer

This analysis is intended solely for educational and informational purposes and does not constitute any investment or financial advice. Past performance is not indicative of future results. All information is sourced from public company filings, analyst reports, and third-party sources believed to be reliable. In accordance with SEBI guidelines, market data is presented with a three-month lag. Investors should conduct independent research, perform due diligence, and consult qualified financial advisors before making any investment decisions. The views expressed are personal and may be subject to errors or bias.

Let’s Talk: Do you see Medi Assist crossing the ATH on execution strength, or do valuations cap the near-term upside? Share your views on its digital moat and insurer partnerships!