Nile Ltd – A Silent Compounder in the Battery Supply Chain?

Low valuation, strong balance sheet, but cyclical growth story to watch closely

Nile Limited is a Hyderabad-based company, operating as a secondary lead manufacturer and recycler, producing pure lead and lead alloys used primarily in lead-acid batteries.

Over time, the company has transformed itself from a niche industrial manufacturer into a critical participant in India’s battery supply chain, processing scrap batteries into refined lead products such as lead calcium, antimony, selenium, and other alloys.

Its operations are supported by two key manufacturing facilities in Andhra Pradesh, with a combined capacity exceeding 100,000 tonnes per annum.

👉 Strategic Insight: Nile is not a consumer-facing brand but an upstream industrial enabler, making it a hidden but essential player in India’s energy storage ecosystem.

Business Profile & Industry Position

Nile operates in the secondary lead recycling and smelting industry, supplying refined lead products to battery manufacturers and industrial clients.

Revenue: ~₹1,000 Cr+ annually

Market Cap: ~₹500 Cr (small cap)

Promoter Holding: ~50%

Capacity: ~107,000+ TPA

India’s battery ecosystem—especially lead-acid batteries—continues to dominate segments like automotive, inverters, and industrial storage.

👉 Positioning Insight: Nile operates in a fragmented but regulated industry, where compliance, scale, and sourcing efficiency create competitive advantages.

Recent Developments

Nile has shown strong operational momentum over recent quarters:

Q1 FY26 profit up ~84% YoY

Q2 FY26 profit up ~38% YoY

Q3 FY26 profit up ~47% YoY

Other key developments include:

NSE trading permission (April 2026) → improved liquidity

Interim dividend declaration → strong cash flows

Windmill PPA expiry → temporary loss of renewable income

Entry into lithium-ion recycling via subsidiary Nile Li-Cycle Pvt Ltd

👉 Interpretation: The company is transitioning from a steady operator to a growth-oriented recycler, with improving profitability and strategic expansion.

Financial Performance Snapshot

Strengths

Profit CAGR ~30% over 5 years

ROCE ~20%, ROE ~14–16%

Near debt-free balance sheet

Strong operating leverage (profit growth > sales growth)

Weakness

Sales CAGR ~11% (moderate growth)

👉 Key Insight: Nile’s earnings growth is driven more by efficiency and margins rather than aggressive revenue expansion.

Market Position & Sales Dynamics

Nile occupies a critical yet largely invisible position within the battery supply chain, with a significant portion of its revenue—around 80–90%—coming from a key customer, Amara Raja Batteries. The broader battery industry is expected to grow at roughly 10% CAGR, providing steady demand support. Additionally, India’s regulatory push through the Battery Waste Management Rules, 2022 is accelerating industry consolidation, driving out informal players and creating stronger growth opportunities for organized and compliant recyclers like Nile.

👉 Sales Insight:

Stable demand driven by battery ecosystem and High dependency risk on key customer

Valuation Analysis (Fundamental View)

P/E ~9.7x → undervalued

P/B ~1.7x → reasonable

Market Cap vs Revenue mismatch → potential re-rating

Long-Term Investment Case

Why Nile Deserves Consideration

Strong balance sheet with minimal debt

Regulatory tailwinds favor organized recyclers

Consistent profit growth trend

NSE listing → visibility and liquidity boost

Early entry into lithium-ion recycling

Structural demand from battery ecosystem

👉 Investment Theme: A slow compounding, value-driven industrial story with optionality from EV recycling.

Risk Factors & Negatives

Customer concentration risk (~80–90% revenue from one client)

Lead price volatility affecting margins

Governance concerns (promoter compensation, related-party loans)

Low scalability due to commodity nature

Competition from backward integration (Amara Raja recycling plant)

Lithium-ion recycling execution risk

👉 Critical Risk: Customer dependency remains the single biggest overhang.

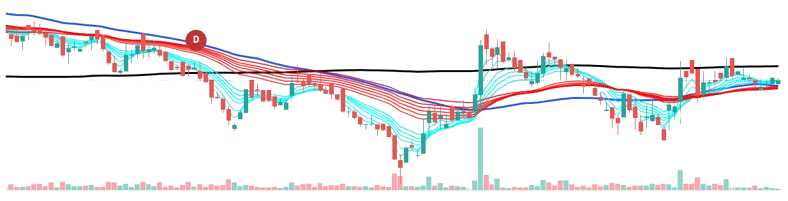

Technical Analysis (Daily Chart Interpretation)

At the current price of around ₹1660, the stock is trading near a key GMMA support zone between ₹1620 and ₹1659, while the 200 DMA at approximately ₹1719 continues to act as an overhead resistance. The RSI at about 53 indicates a neutral momentum, suggesting neither overbought nor oversold conditions. In the medium term, the stock is likely to remain range-bound, with a breakout above ₹1720–1750 signaling bullish momentum. From a long-term perspective, the stock appears to be in a Stage 1 accumulation phase, with the potential to move higher if supported by improving fundamentals and sustained earnings growth.

👉 Technical Insight: Stock is in a base-building phase with early signs of trend reversal

Overall Investment Thesis

Nile Ltd presents a balanced investment proposition by combining value (low P/E), financial stability (debt-free balance sheet), and future growth optionality through its foray into EV and lithium-ion battery recycling. However, its growth profile remains moderate and cyclical due to the nature of its commodity-linked business. As a result, the stock is better positioned to deliver steady compounding returns in the range of 12–18% over the long term, rather than high-growth multibagger returns—unless supported by a meaningful valuation re-rating or strong structural triggers.

Conclusion & Final Take

Nile Ltd represents a quiet, fundamentally sound, and undervalued industrial business operating at the intersection of recycling, battery demand, and favorable regulatory shifts. While it may not offer aggressive growth triggers, it makes up for this through strong financial discipline, consistent margin expansion, and a well-positioned role in a critical supply chain. The stock is best suited for long-term value investors and as part of a diversified portfolio, but may not appeal to those seeking momentum-driven or high-growth opportunities.

Accumulate gradually with patience; this is a slow compounder with potential upside from sector tailwinds and valuation re-rating.

Street Sentiment Snapshot – Nile Ltd. (Source: Investor Forums)

Investor discussions on public forums (e.g., Moneycontrol) reflect a constructively bullish bias on Nile Ltd., with the stock increasingly being perceived as an undervalued play on the recycling and EV ecosystem. However, this optimism is accompanied by notable concerns around execution and governance.

Key Positives Highlighted by Investors:

Liquidity Upside: The anticipated benefits from an NSE listing are expected to enhance trading volumes and improve price discovery.

Earnings Momentum: Strong recent quarterly performance (notably Q3) with improvement in net profit and EPS has reinforced confidence in the business trajectory.

Institutional Interest: Reported participation from FIIs and Alternate Investment Funds is seen as a validation of the company’s long-term prospects.

Valuation Gap: The stock is widely viewed as trading at a discount to peers, suggesting potential for re-rating.

Structural Tailwinds: Increasing demand for battery recycling, particularly driven by EV adoption, positions the company favorably within a high-growth segment.

Corporate Actions Optionality: Expectations around potential bonus issues, stock split, and subsidiary listing are perceived as triggers for value unlocking.

Market Expectations & Price Narratives:

Short-term sentiment reflects expectations of meaningful upside, supported by improving liquidity and recent earnings momentum.

Medium- to long-term narratives remain strongly optimistic, driven by anticipated execution improvements and favorable sector tailwinds.

Some participants also point to low free float, which may amplify price volatility and contribute to perceived price inefficiencies.

Key Risks & Concerns:

Input Cost Volatility: Fluctuations in raw material prices could impact margins.

Customer Concentration: Dependence on a key client such as Amara Raja Batteries raises concentration risk.

Market Conduct Risks: Concerns around potential price manipulation due to limited float remain a recurring theme in discussions.

Expectations from Management:

Investors are urging faster execution of capacity expansion plans to capitalize on sectoral growth opportunities.

There is also discussion around international expansion, including potential operations in South Africa, which could diversify revenue streams.

While informal investor sentiment remains decisively positive, the narrative is heavily influenced by expectations of future triggers and sectoral growth. From a research standpoint, these views should be treated as indicative rather than definitive, with due consideration given to underlying fundamentals, execution capability, and risk factors.

Disclaimer

This analysis is intended solely for informational purposes and does not constitute any investment or financial advice. All information is sourced from public company filings, analyst reports, and third-party sources believed to be reliable. In accordance with SEBI guidelines, market data is presented accordingly. Investors should conduct independent research, perform due diligence, and consult qualified financial advisors before making any investment decisions. The views expressed are personal and may be subject to errors or biases.