NSDL – India’s Depository Colossus

Structural Growth Story Amid Short-Term Technical Weakness

Investment Summary

National Securities Depository Limited (NSDL), India’s largest and first depository, is a core pillar of the country’s capital market infrastructure. Despite a ~25% correction from its post-IPO peak, its long-term fundamentals remain strong, supported by rising financialization, growing equity participation and digital asset adoption. With dominant custody share, high recurring revenues, an asset-light, debt-free model and strong scalability, NSDL stands out as a structural compounder. However, elevated valuations and short-term technical weakness make phased accumulation the preferred strategy.

Company Overview

NSDL, incorporated in 2012 and the pioneer of India’s dematerialization system, is the country’s largest depository by custody value. It holds an 86.6% market share, manages ₹511 lakh crore of assets, services 4.19 crore demat accounts, and operates through over 65,000 centres covering 99% of Indian pin codes with global reach across 186 countries. Listed in August 2025 at ₹890, the stock now trades near ₹1,070, valuing the company at about ₹21,400 crore with a book value of ₹108 per share. Operations are supported by NDML and NSDL Payments Bank, in which NSDL has recently diluted a small stake to improve capital efficiency.

Financial & Operating Performance

In Q2 FY26, NSDL reported ₹250 crore of total income, reflecting 18.9% year-on-year growth, while PAT rose 18% to ₹120 crore. EBITDA margin stood near 24% and PAT margin at over 22%, highlighting excellent operating leverage.

Over the long term, NSDL has delivered strong compounding:

Revenue has grown at a 34% CAGR over five years

Profit has grown at a 21% CAGR over five years

Trailing twelve-month profit growth stands at 25%

The balance sheet remains extremely strong, with total borrowings of only ₹19 crore, making the company virtually debt-free.

Operational Leadership

NSDL has made significant progress in the retail demat segment. Its retail market share has doubled from 9.40% to 15.50% within one year, and its share in new account additions has jumped to 17.60% in Q2 FY26, reflecting accelerating retail traction.

In unlisted securities, NSDL enjoys commanding dominance with over 73% market share, more than 11,500 unlisted issuers onboarded, and a total issuer base exceeding one lakh companies on its network.

Revenue visibility remains exceptionally high as over 85% of revenue is recurring, coming from annual maintenance charges, custody and settlement fees, institutional services, corporate actions, e-voting, KYC and e-governance services.

Industry Tailwinds

India’s depository industry is undergoing a multi-year structural expansion. Demat accounts have grown from around 2.5 crore in 2016 to nearly 21 crore by 2025. The industry is expected to grow at 15–20% CAGR through 2030, supported by increasing retail participation, rapid digitalisation of assets, fintech-broker integrations, faster T+1 settlement cycles, and strong growth in unlisted, REIT, InvIT and alternative investment markets. NSDL also dominates high-value NRI and FPI accounts, positioning it as the preferred institutional gateway.

Competitive Positioning – NSDL vs CDSL

NSDL commands leadership in custody value, unlisted markets, institutional and FPI accounts. While CDSL enjoys a higher retail market share and superior ROE metrics, NSDL trades at relatively lower price-to-book multiples despite handling significantly larger asset custody, indicating a relatively balanced valuation for a structural infrastructure asset.

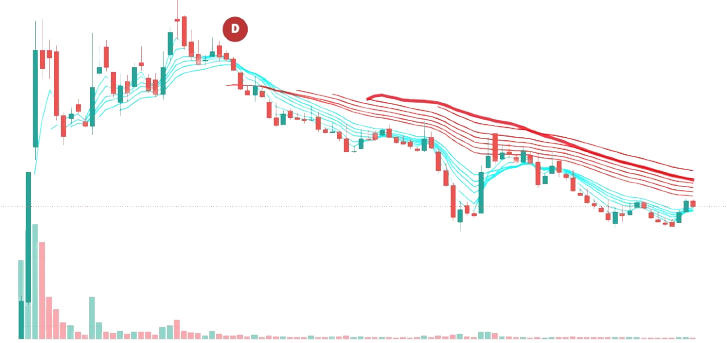

Valuation & Technical View

At current levels, NSDL trades at around 62x earnings and 10x book value. These elevated multiples reflect its dominant market position, strong recurring revenue profile, asset-light scalability and structural growth visibility.

Technically, the stock remains in a consolidation phase after correcting roughly 25% from its post-listing peak of ₹1,425. The ₹1,000–1,050 zone represents a strong long-term support band, while ₹1,150–1,250 remains a key resistance area. Near-term consolidation is likely before the next sustained trend emerges.

SWOT Overview

NSDL’s key strengths lie in its dominant market leadership, high switching costs, strong institutional relationships, asset-light scalability and a debt-free balance sheet with pan-India reach. Its primary weaknesses are lower retail market share compared to CDSL, relatively modest ROE and premium valuation multiples. Growth opportunities stem from the ongoing financialization of household savings, rapid expansion in unlisted securities, fintech integrations, and the emergence of digital and tokenised asset classes. Key threats include regulatory changes, cybersecurity risks, technological disruption and increasing pricing competition in the retail demat segment.

Growth Outlook

Over the next one to two years, NSDL is expected to deliver 12–15% revenue growth and 18–22% PAT growth, driven mainly by retail share expansion and operating leverage.

Over the medium term, revenue CAGR is projected at 15–18%, with profit CAGR of 20–25%, aided by margin expansion, new asset classes and fintech integrations.

Over the long term, NSDL has the potential to evolve into a ₹50,000+ crore market capitalisation company and emerge as a comprehensive digital financial infrastructure platform.

Investment Conclusion

NSDL represents a rare opportunity to invest in India’s financial market backbone. Its dominant moat, debt-free balance sheet, predictable recurring revenue and accelerating retail participation make it a high-quality structural compounder.

Given rich valuations and near-term technical consolidation, the stock is best accumulated on dips in the ₹1,000–1,050 zone, with a long-term investment horizon.

Strategy: BUY ON DIPS – Long-term wealth creation potential remains intact.

Disclaimer

This analysis is intended solely for informational purposes and does not constitute any investment or financial advice. All information is sourced from public company filings, analyst reports, and third-party sources believed to be reliable. In accordance with SEBI guidelines, market data is presented accordingly. Investors should conduct independent research, perform due diligence, and consult qualified financial advisors before making any investment decisions. The views expressed are personal and may be subject to errors or bias.

Valuable information.