Pace Digitek Ltd: Powering India’s Digital Infrastructure Revolution

A Compelling Growth Story in Telecom Infrastructure & Renewable Energy Storage

Pace Digitek is a fast-growing player at the intersection of India’s expanding telecom infra and the high-potential battery energy storage (BESS) market. The company maintains strong earnings momentum, backed by a robust ₹8,500+ crore order book offering 18–24 months of revenue visibility. With FY25 revenue of ₹2,440 crore and ROE of 31% ROCE 41%, the company is well-positioned to capture opportunities from 5G rollout, BharatNet expansion, and India’s energy transition.

BUSINESS VERTICALS

Pace Digitek’s business is anchored by its Telecom Infrastructure division, which contributed 94% of FY25 revenue through telecom tower deployment, DC power systems, OFC laying, and comprehensive O&M services, supported by strong involvement in India’s 5G rollout.

Its Energy Solutions segment accounted for 5% of revenue, covering Battery Energy Storage Systems (BESS), lithium-ion battery manufacturing, hybrid DC systems, and solar and rural electrification projects—an area with significant future growth potential.

The company’s ICT Services segment, contributing less than 1%, includes surveillance systems, smart classrooms, and remote monitoring solutions.

CAPACITY & FOOTPRINT

Three Bengaluru manufacturing units (200,000 sq. ft., ISO & CMMi L3)

2.5 GWh BESS manufacturing facility at Bidadi (commissioned Apr 2025)

Global reach: Myanmar, Africa, Sri Lanka, Bangladesh, Philippines.

RECENT DEVELOPMENTS

SECI BESS Project – ₹1,159 crore

600 MW/1,200 MWh standalone grid BESS project in Andhra Pradesh with 10-year O&M.Tata Teleservices – ₹186 crore (3.5 years)

Managed OSP fiber & ISP operations across five southern states.Maharashtra BESS Project – ₹750 crore

750 MW/1,500 MWh storage across 75 substations on BOO basis.

FINANCIAL PERFORMANCE - FY2025

Revenue: ₹2,440 crore: Net Profit: ₹279 crore (+21.4% YoY)

Net Debt: ₹161 crore (D/E 0.14x)

Q2 FY2026

Revenue: ₹367 cr (+7.28% YoY, –46% QoQ): Net Profit: ₹55 cr (+10% YoY)

Decline QoQ due to project-based lumpiness; annual trend intact.

INDUSTRY DRIVERS & OUTLOOK

1. 5G & BharatNet Expansion

Telecom infra expected to grow to ₹2.0–2.1 trillion (FY23–28), driven by densification of 5G networks and rural broadband (BharatNet Phase-III).

2. Energy Storage Boom

India’s BESS capacity to expand from 34,720 MWh (2022–27) to 201,500 MWh (2027–32). Government mandates and renewable integration boost demand.

3. Policy Tailwinds

PLI for telecom & energy storage, National Solar Mission (500 GW by 2030), Smart Cities, and Make in India enhance sectoral opportunities.

4. Strong Operating Leverage

Backward integration, new BESS unit and annuity AMC contracts improve margins and cash flows.

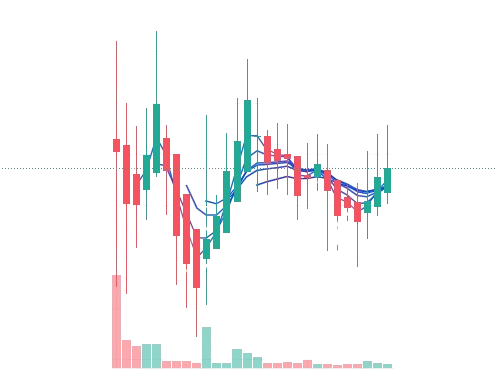

TECHNICAL VIEW

Pace Digitek firmly supported by both the 50-day and 200-day SMAs and RSI remains neutral at 51, indicating balanced momentum, the price action is forming a bullish flag/pennant pattern that reflects steady accumulation. Overall, the stock is in a late Stage 1 basing phase with early signs of a transition into Stage 2, supported by tight consolidation a strong breakout with rising volume would confirm the start of a Stage 2 uptrend and open the path for the next bullish move.

CONCLUSION

Pace Digitek stands out as a high-conviction structural growth story, leveraging India’s digital and clean energy transformation. With over ₹8,500 crore in orders, rising BESS exposure, strong balance sheet, and expanding capacities, the company is positioned for 25–30% CAGR over FY26–28 and offers asymmetric upside for investors focused on India’s telecom and renewable energy megatrends.

Disclaimer

This analysis is intended solely for educational and informational purposes and does not constitute any investment or financial advice. All information is sourced from public company filings, analyst reports, and third-party sources believed to be reliable. Investors should conduct independent research, perform due diligence, and consult qualified financial advisors before making any investment decisions. The views expressed are personal and may be subject to errors or bias.