Pumping Through the Pain: Is Oswal Pumps a Future Multibagger?

Deep-dive into fundamentals, risks, and the evolving base formation story

Oswal Pumps Ltd is one of India’s fastest-growing vertically integrated solar pump manufacturers, offering complete solar irrigation solutions that include pumps, motors, controllers, and solar modules. Incorporated in 2003, listed in June 2025 and currently operates with a market Cap of ₹4,200 Cr.

The company sits at a strategic intersection of renewable energy and agriculture, driven largely by the government-backed PM-KUSUM scheme, which aims to accelerate solar-powered irrigation adoption across India.

Financial Performance Snapshot

The company has demonstrated a clear hyper-growth trajectory over the past few years, with revenue expanding sharply from ₹360 Cr to ₹1,430 Cr in FY25 and further to ₹1,900+ Cr on a TTM/FY26E basis. Profit growth has also remained strong, increasing from ₹280 Cr to ₹340+ Cr, with FY25 profit surging by approximately 159% year-on-year. This robust financial performance reflects strong execution capabilities and favorable demand tailwinds in the solar irrigation segment. Profitability metrics are equally impressive, particularly for a capital goods company, with EBITDA margins in the range of 25–30%, ROE of around 87%+, and ROCE of approximately 78%+. Collectively, these indicators position Oswal Pumps among the top-tier performers in its sector.

Market Position & Competitive Strength

Oswal Pumps holds a dominant ~38% market share under the PM-KUSUM scheme, supported by a robust distribution network of over 1,000 distributors. Its vertically integrated model provides cost efficiencies and margin stability.

Expansion & Growth Initiatives

The company is undertaking significant capacity expansion to support its future growth, with pump manufacturing capacity being scaled up from 2 to 5 lakh units per year. In parallel, its solar module capacity is planned to increase substantially from 570 MW to 2,200 MW by 2028, reflecting a strong commitment to backward integration and long-term scalability.

Order Book Highlights

The company has built a strong and diversified order pipeline, including projects worth ₹380 Cr from Maharashtra, ₹180 Cr from MSEDCL, and over ₹240 Cr from Karnataka. This robust order book provides clear forward revenue visibility and underpins confidence in the near- to medium-term growth trajectory.

Valuation Analysis

Despite strong growth, the company’s valuation remains relatively attractive, with the stock trading at a P/E of around 12× compared to the industry average of approx 38× and an EV/EBITDA multiple of about 24×. This indicates that the stock is currently priced below sector averages, offering a degree of valuation comfort and potential upside.

Forward Outlook

The company’s valuation is expected to become even more attractive if growth sustains and a PEG ratio of less than 1 reinforces the investment case, indicating a favorable balance between growth and valuation and supporting the thesis of growth at a reasonable price.

Key Rating Drivers - Strengths

Oswal Pumps benefits from a well-established market position built on over three decades of promoter experience in the water pump industry. The company has developed a diversified product portfolio and a strong distribution network and OEM relationships, ensuring consistent order flow. Its transition into a fully integrated solar pump solutions provider under the PM Kusum Yojana has further strengthened its positioning. Revenue has grown at a CAGR of 54% up to FY25 and is expected to reach ₹1,700–2,000 crore in FY26, with continued growth of 20–25% supported by a strong order book of almost ₹1,058 crore and favorable government policies.

Sound Operating Profitability

The company has demonstrated strong improvement in operating profitability, driven by higher contribution from solar pumps, increased direct participation in government projects, backward integration, and scale benefits. Operating margins expanded significantly to 29.5% in FY25 from 20% in FY24 and are expected to sustain at healthy levels of 26–27% over the medium term, supported by its leadership in the agri-solar segment and continued efficiency gains.

Healthy Financial Risk Profile

Oswal Pumps maintains a healthy financial profile, with net worth estimated at ₹1,400–1,600 crore post-IPO. Despite some increase in working capital debt, the overall capital structure remains comfortable, supported by strong internal accruals and low reliance on term debt. Key metrics such as total outside liabilities to net worth (0.3–0.4x), interest coverage (11–13x), and cash accrual to debt (1–1.1x) indicate robust financial stability. Going forward, the financial profile is expected to remain stable due to healthy profitability and limited dependence on debt-funded capex.

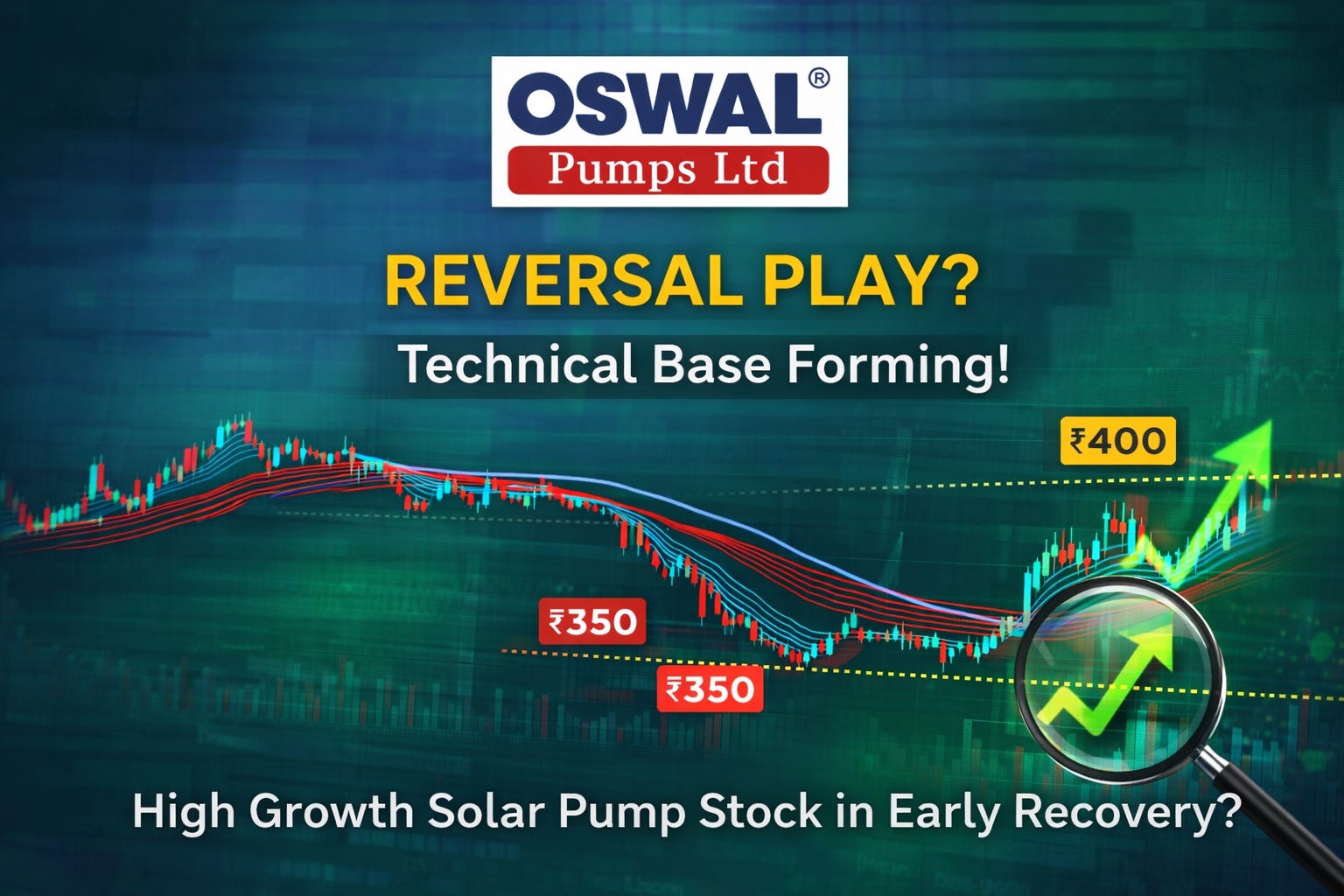

Technical Analysis and Trend Status (Chart Insight)

The stock has corrected sharply, declining by approx. 58% from its peak levels of ₹900–950 and continues to trade below key moving averages, including the 50 DMA and 200 DMA.

Current Structure: Base Formation

Recent price action suggests early signs of stabilization, with the stock consolidating in this range. Key technical signals include the formation of higher lows, compression in the GMMA bands, and a noticeable pickup in volumes at lower levels. Together, these indicators point toward a potential accumulation phase, likely driven by informed investors positioning ahead of a possible trend reversal.

Outlook: Medium-Term

Over the medium term, the stock is likely to consolidate within the ₹320–450 range, as it continues to build a base after the recent correction. A key trigger to watch is a breakout accompanied by strong volumes, which could signal the start of momentum. A more decisive trend reversal would be confirmed only on a sustained move above current levels BUT until such confirmations emerge, the overall stance remains that of cautious accumulation.

Outlook: Long-Term

The long-term investment story for the company remains structurally strong, supported by its market leadership under the PM-KUSUM scheme, advantages from vertical integration, and a robust order pipeline coupled with ongoing capacity expansion. At current levels of around, the stock is trading below its historical valuation averages, making it an attractive entry zone for patient investors willing to ride out near-term volatility.

Investment Positives

Strong revenue and profit growth

High-margin, efficient business model

Leadership position in PM-KUSUM

Structural tailwinds (solar + agriculture)

Key Risks & Concerns

The company faces several risks across business, financial, operational, and market dimensions. A significant concern is its heavy dependence on the PM-KUSUM scheme, contributing 85–87% of revenue, along with geographic concentration in Haryana and Rajasthan. Financially, high receivables and negative operating cash flows remain key challenges.

Operationally, margins have seen some compression (29% to 26% on annual basis), and there is an auditor flag related to the ERP audit trail. From a market perspective, the stock continues to trade below its 200 DMA, and the sharp correction has weakened overall investor sentiment.

Final Investment View

Oswal Pumps presents a rare divergence opportunity:

Fundamentals: Strong and improving

Price Action: Deep correction

Technicals: Early base formation

This combination creates a potential accumulation zone for investors with a medium- to long-term horizon.

Strategy Insight

Aggressive Investors: Accumulate gradually

Conservative Investors: Wait for breakout above ₹400–420

Conclusion

Oswal Pumps is currently at a critical inflection point:

Past: Sharp correction

Present: Base formation

Future: Potential re-rating candidate

If the company sustains growth, improves cash flows, and benefits from continued policy support, it has the potential to evolve into a high-quality small-cap compounder over the next few years.

Disclaimer

This analysis is intended solely for informational purposes and does not constitute any investment or financial advice. All information is sourced from public company filings, analyst reports, and third-party sources believed to be reliable. In accordance with SEBI guidelines, market data is presented accordingly. Investors should conduct independent research, perform due diligence, and consult qualified financial advisors before making any investment decisions. The views expressed are personal and may be subject to errors or biases.

💬 Let Us Talk

Do you see this as a value buy or a value trap at current levels? Are you waiting for confirmation above ₹400 or accumulating early? Drop your view 👇