🔥 RAMKRISHNA FORGINGS: FORGED IN STRENGTH, TESTED BY TURBULENCE

Can This Midcap Titan Overcome Inventory Woes and Debt Challenges?

🏭 COMPANY SNAPSHOT

Ramkrishna Forgings - India's forging giant with a 4-decade legacy, commanding 62% market share in India's forged components sector. From humble beginnings in 1981 to becoming a global supplier serving 22 countries, RKFL has built an empire in the metal forging industry.

Key Metrics Overview (June 2025)

RKFL holds a market capitalization of ₹12,031 crore, with its stock priced at ₹660.50, within a 52-week range of ₹553 to ₹1,064.

The company operates a substantial production capacity of 268,400 metric tons annually and has a global footprint, exporting to 22 countries, primarily North America and Europe.

Its prestigious client base includes industry leaders such as Tata Motors, Volvo, Scania, and Indian Railways.

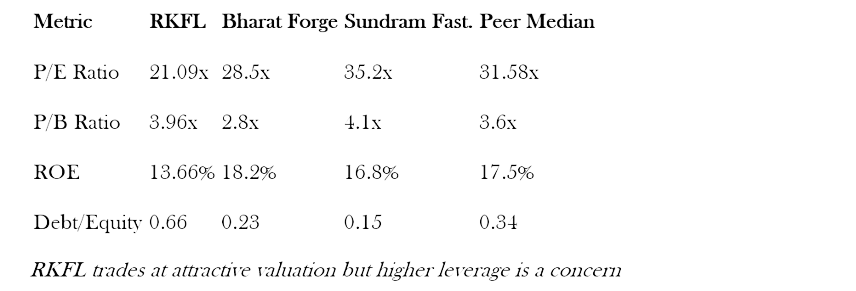

Valuation Metrics

RKFL presents an attractive investment case with a P/E ratio of 21.09x, notably below the peer median of 31.58x, indicating potential undervaluation.

The P/B ratio stands at 3.96x, reflecting a reasonable book value multiple. However, its EV/EBITDA of 27.3x suggests a premium valuation, justified by RKFL’s strong market position.

The debt-to-equity ratio has improved significantly to 0.66 from 1.48 in FY22, highlighting enhanced financial stability.

Performance Indicators

The company’s return on equity (ROE) for FY25 is 13.66%, while its return on capital employed (ROCE) has declined to approximately 7% (restated FY25) from 16–17% in FY24, signaling profitability challenges.

RKFL maintains a conservative dividend yield of 0.30%, and its beta of 1.07 indicates moderate volatility relative to the market.

💰 FINANCIAL PERFORMANCE DEEP DIVE

The Growth Story

Revenue CAGR: 33% (FY21-25) - Exceptional top-line growth

Order Book: ₹4,600 crores in FY25 - Strong revenue visibility

Capacity Expansion: Added 56,000-tonne forging press line

The Challenges

Operating Margin: Dropped to 13.9% (from 20-22%) post-restatement

Free Cash Flow: Consistently negative due to capex-intensive expansion

Debt Surge: Borrowings at ₹2,013 crores (Net Debt/EBITDA: 3.5x)

Recent Quarterly Trends

Q1 FY26: Revenue ₹959 Cr, OPM 14.8%, PAT ₹81 Cr

Q2 FY26: Revenue ₹1,077 Cr, PAT ₹21 Cr (11% QoQ decline)

Q3 FY26: Revenue ₹959 Cr, PAT ₹100 Cr (202% YoY growth)

🏰 THE MOAT ANALYSIS

Competitive Advantages

✅ Market Leadership: 2nd largest forging company in India ✅ Global Footprint: 40% export revenue from premium markets ✅ Technology Edge: Advanced warm & cold forging capabilities ✅ High Entry Barriers: Capital-intensive, relationship-driven business

Strategic Positioning

Client Concentration: 50-55% revenue from top 5 clients

Geographic Spread: Balanced domestic-export mix

Sector Diversification: Reducing auto dependency

🚨 THE ELEPHANT IN THE ROOM: INVENTORY ISSUE

The Controversy

₹202.6 Crore Inventory Overstatement - A forensic audit bombshell

Net Worth Impact: Eroded by 6.73%

Margin Restatement: OPM reduced from >20% to 13.9%

Credibility Crisis: CRISIL Rating Watch with Negative Implications

🎭 MANAGEMENT COMMENTARY

"The inventory issue was a one-time event due to process gaps. We've implemented robust controls and promoter commitment shows our confidence in the business." - Management

Key Commitments

Promoter fund infusion within FY26

SAP system overhaul by September 2025

Return to 20%+ EBITDA margins by FY26-27

Debt reduction through improved cash flows

👥 SHAREHOLDING PATTERN: WHO'S BETTING ON RECOVERY?

Current Holdings (March 2025)

Promoters: 43.13% (Stable with warrant commitment)

FIIs: 24.48% (↑ from 24.04%)

DIIs: 6.0% (↑ from 5.41%) - Growing institutional confidence

Key Observations

Promoter Pledging: 5.76% (marginal improvement)

Institutional Interest: DIIs increasing stake

Warrant Issuance: Promoters committed to infuse ₹204.75 crores through 975,000 warrants at ₹2,100 per share - well above current market price, showing skin in the game.

🚀 FUTURE CATALYSTS & GROWTH DRIVERS

Management Guidance FY26

Revenue Growth: 15-20% expected

EBITDA Margin: Gradual recovery to 20%+ by FY26-27

Capex Reduction: Sharply reduced to ₹100-150 Cr

Debt Reduction: Through cash flows and promoter infusion

Strategic Initiatives

🚄 Railway Boom: Fully assembled bogie frames contract 🌎 Mexico Expansion: 10-year USD 3.5M annually contract 🏭 Chennai Wheel Plant: ₹2,000 Cr investment for FY27 revenues 📈 Non-Auto Growth: Target 25% of revenue in 3-4 years

⚠️ RISK ASSESSMENT

❌ Governance Concerns: Inventory scandal impact on credibility ❌ Debt Burden: High leverage with refinancing risks ❌ Customer Concentration: Over-dependence on top clients ❌ Cyclical Exposure: Auto sector volatility

Mitigation Factors

✅ Promoter Commitment: Premium warrant pricing ✅ Diversification: Expanding non-auto portfolio ✅ Process Improvements: SAP automation ✅ Financial Discipline: Reduced capex plans

🎯 KEY TRIGGERS TO WATCH

Positive Catalysts

✅ Successful promoter fund infusion ✅ Margin recovery to 18%+ levels ✅ Debt reduction below ₹1,500 Cr ✅ Major railway order wins ✅ Export business acceleration

Red Flags

❌ Further inventory/accounting issues ❌ Promoter fund infusion delays ❌ Continued margin compression ❌ Rating downgrades

📈 TECHNICAL OUTLOOK

Current Status

Price: ₹660.50 (June 11, 2025)

52-Week Performance: -32.5% (Down from ₹1,064 high)

Momentum: Neutral to bullish - Chart showing a reversal - Assuming successful turnaround

🏁 FINAL VERDICT: THE MOMENT OF TRUTH

**Yahoo Finance India analysis**

The Investment Thesis

Ramkrishna Forgings represents a classic turnaround story. The company's four-decade legacy in forging excellence faces its biggest test with the governance crisis. However, the fundamentals remain compelling:

🎬 CONCLUSION: THE COMEBACK STORY IN MAKING?

Ramkrishna Forgings isn't just a stock story - it's a test of corporate resilience. The company that helped build India's forging industry is now fighting to rebuild investor trust.

The Investment Thesis

Ramkrishna Forgings represents a classic turnaround story. The company's four-decade legacy in forging excellence faces its biggest test with the governance crisis.

The Verdict

This isn't a quick trade - it's a long-term bet on India's infrastructure story and management's ability to execute. With patience and proper risk management, RKFL could script a remarkable comeback story.

However, caution is paramount. The inventory scandal has shaken the foundation of trust, and only consistent execution can rebuild it.

⚖️ DISCLAIMER

This newsletter is for informational purposes only and not a recommendation to buy or sell securities. Investors should consult a financial advisor before making decisions. Past performance is not indicative of future results, and stock prices are subject to market risks.

📞 LET'S TALK

What's your take on RKFL's recovery prospects?

Do the promoter's ₹204.75 crore infusion and new orders outweigh the inventory scandal?

How does RKFL stack up against peers like Bharat Forge?

Is the current valuation attractive enough to justify the governance risks?

Join the discussion and share your thoughts on this compelling turnaround story!