Savita Oil Technologies — Powering India’s Energy Infrastructure Transition

India’s Silent Transformer Oil Giant Emerging as a Specialty Energy-Fluid Player in the Transformer, Renewable Energy & Grid Modernization Boom

Savita Oil Technologies Limited is emerging as a key beneficiary of India’s expanding power infrastructure, renewable energy, and transformer manufacturing boom. Traditionally seen as a cyclical lubricant and petroleum company, Savita is gradually transforming into a specialty energy-fluid and thermal-management solutions player. Strong transformer oil demand and sharp price increases during early 2026 have significantly improved the company’s earnings outlook, supported by its nearly 33% domestic market share in transformer oils.

FY - 2026 marked a strong turnaround with record revenues, improving margins, and historic annual volumes crossing 5,00,000 KL. The company’s long-term growth potential lies in high-margin ester-based transformer fluids and advanced specialty applications linked to renewable energy and energy storage systems.

Savita offers strong market leadership, improving profitability and a near debt-free BS, investors should remain mindful of risks arising from crude oil volatility and commodity-linked business cycles.

Industry Opportunity & Structural Tailwinds

India is undergoing a massive power infra expansion driven by renewable energy growth, transmission upgrades, rail electrification, smart grids, data centers, and rising industrial electricity demand. As transformer oil is an essential component in power transformers, companies like Savita Oil stand to benefit directly from this long-term structural trend.

Key growth drivers include renewable energy integration, grid modernization, energy storage systems, EV infra and expanding transmission & distribution networks. India’s ambitious target of achieving 500 GW renewable energy capacity by 2030 further strengthens the multi-year demand outlook for transformers and specialty insulating fluids.

Global Transformer Oil Market

The global transformer oil market is witnessing steady growth driven by rising electrification, renewable energy investments, and expanding power infrastructure worldwide. Key industry trends include increasing demand for bio-based and fire-safe ester fluids, stronger ESG compliance requirements, and growing adoption of advanced cooling solutions for modern energy systems.

Asia-Pacific remains the largest and fastest-growing market, with India emerging as one of the key growth drivers due to its rapid power and renewable infrastructure expansion.

Recent Developments & FY2026 Performance

FY - 2026 marked a significant turnaround year for Savita Oil Technologies. After margin pressure and earnings weakness during FY - 2025 due to crude and base oil volatility, the company delivered strong recovery in revenues, profitability, and operating performance.

Some of the Key FY - 2026 Highlights are as follows:

Revenue crossed approximately ₹4,400 crore and Profit before tax surged sharply year-on-year

Annual volume crossed 5,00,000 KL for the first time

Double-digit growth reported in transformer oils and exports, Operating leverage improved significantly and EBITDA margins expanded meaningfully

Strategic Corporate Developments

Savita GreenTec Merger: Savita approved amalgamation of Savita GreenTec into the parent entity. This move simplifies the corporate structure and strengthens integration of renewable-energy-related operations.

Governance Improvements: The appointment of Ernst & Young as internal auditor reflects management’s intent to improve governance standards and operational systems.

Shareholder-Friendly Capital Allocation: Savita has consistently maintained dividend payouts and also approved a share buyback previously, reflecting balance-sheet strength and management confidence.

Business Economics & Margin Dynamics

Understanding Savita’s economics is extremely important because the business model differs significantly from typical high-margin specialty chemical companies.

Raw Material Sensitivity

Approx 85–90% of Savita’s input costs are linked to imported base oils, making profitability highly sensitive to crude oil price movements. As a result, inventory management and pricing power play a critical role in determining margins. Sharp crude corrections can lead to inventory losses, while sudden price spikes may temporarily compress profitability until costs are passed on to customers.

Historically, this dependence on volatile raw material prices has contributed to cyclical fluctuations in the company’s earnings and margins.

Why FY - 2026 Appears Different

FY - 2026 appears structurally stronger as demand across the transformer ecosystem has accelerated significantly, driven by renewable energy expansion, transmission capex, strong order inflows, and faster replacement cycles. Tight supply conditions have improved pricing realizations, inventory turnover, operating leverage, and overall earnings visibility for Savita Oil Technologies.

The sharp rise in transformer oil prices during early 2026 further highlights the intensity of demand within the power infrastructure sector.

Ester Fluids — The Key Long-Term Growth Driver

The biggest long-term opportunity for Savita lies in ester-based transformer fluids and specialty thermal-management solutions. Unlike traditional mineral transformer oils, ester fluids offer higher margins, better fire safety, superior thermal performance, environmental sustainability, and strong ESG alignment, making them increasingly preferred in renewable energy and modern power infrastructure applications.

Future demand could be driven by renewable energy transformers, battery storage systems, immersion cooling for data centers, EV cooling and advanced industrial thermal management. Successful scaling of this segment could gradually transform Savita from a commodity-linked petroleum business into a higher-quality specialty energy-fluid company, improving margins, return ratios, earnings quality, and long-term valuation potential.

Financial & Valuation Perspective

Savita Oil appears reasonably valued compared with many specialty chemical and energy-transition companies, especially considering its improving earnings trajectory and strong market position. The company benefits from a near debt-free balance sheet, healthy cash generation, positive free cash flows, and strong promoter ownership, providing financial stability across business cycles.

At current valuations, the stock trades at relatively moderate levels versus specialty peers, with balance-sheet strength offering downside support. However, a meaningful long-term rerating will likely depend on sustained earnings growth, expansion of higher-margin specialty products, successful scaling of ester fluids, margin improvement, and stronger return ratios over time.

Technical & Market Perspective

The stock’s recent technical structure also supports improving market sentiment.

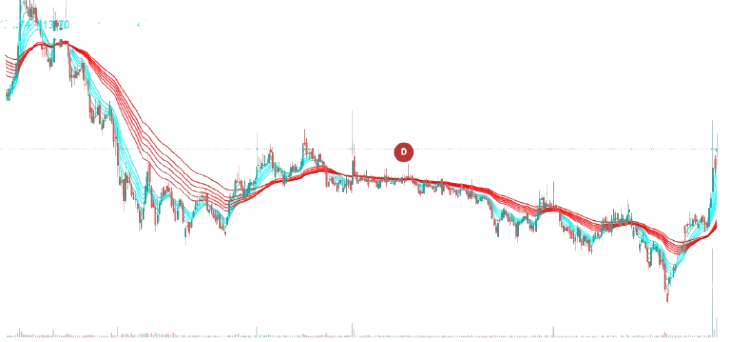

Observations from Daily Chart Analysis

Savita Oil Technologies remained in a prolonged consolidation phase for nearly 12–14 months before witnessing a strong breakout during March–May 2026. The stock reclaimed key moving averages with rising volumes, indicating improving momentum and strengthening market sentiment. The breakout structure, supported by higher trading activity, suggests increasing institutional participation and the possibility of a medium-term trend reversal.

The stock rallied sharply from lower levels, indicating renewed investor confidence in the earnings cycle.

Medium-Term Outlook

If the current transformer demand cycle sustains, Savita Oil could continue witnessing earnings upgrades, improving market sentiment, and stronger institutional interest. Growing traction in specialty and ester-based fluids may further strengthen the company’s long-term rerating potential.

However, short-term volatility may persist due to fluctuations in crude oil prices, commodity cycles, and broader market corrections, which can temporarily impact margins, sentiment, and stock performance.

Key Investment Positives

Market Leadership in Transformer Oils: Savita Oil holds an estimated ~33% domestic market share, positioning it as a key beneficiary of India’s growing transformer demand cycle.

Structural Power Infra Tailwinds: Strong exposure to renewable energy, grid expansion, transmission upgrades, and electrification supports long-term demand growth.

High-Growth Specialty Products: Expansion into ester-based fluids and thermal-management solutions could improve margins and overall business quality over time.

Strong Financial Position: Near debt-free balance sheet and healthy cash flows provide financial stability and strategic flexibility.

Improving Earnings Momentum: FY - 2026 marked a strong recovery in revenues, margins, and profitability after a challenging FY - 2025.

Global Export Presence: Operations across 75+ countries provide diversification and long-term growth opportunities.

Shareholder-Friendly Management: Consistent dividends, buybacks, and strong promoter holding reflect aligned long-term management interests.

Risks & Key Concerns

Raw Material Volatility: Since base oils form the majority of input costs, fluctuations in crude oil prices can significantly impact margins and profitability.

Commodity-Linked Business Model: Traditional transformer oils remain relatively commodity-driven, making long-term rerating dependent on growth in higher-margin specialty products.

Business Cyclicality: Performance remains sensitive to power capex trends, industrial demand, oil price cycles, and broader global economic conditions.

Moderate Margin Profile: Compared with pure specialty chemical companies, Savita continues to operate with relatively moderate operating margins.

Execution Risk: Future growth depends on successful scaling of ester-based fluids, specialty products, and advanced thermal-management solutions.

Export & Logistics Exposure: Freight disruptions, geopolitical tensions, and global supply-chain challenges can temporarily affect export profitability and operations.

Long-Term Outlook & Final Assessment

Savita Oil appears to be entering an important strategic phase as it gradually transitions from a cyclical petroleum products company into a specialty energy-fluid and thermal-management player and is well positioned to benefit from long-term structural themes such as renewable energy expansion, grid modernization, transformer demand growth, rail electrification, data centers, energy storage systems, and advanced cooling applications.

If management successfully scales its specialty and ester-fluid business, Savita could achieve:

Better earnings consistency

Higher operating margins

Improved return ratios

Stronger institutional participation

Gradual valuation rerating

At current valuations, the stock offers a balanced risk-reward profile for investors comfortable with commodity-linked volatility. With strong market leadership, improving earnings momentum, financial strength, and exposure to India’s power infrastructure and energy-transition cycle, Savita may emerge as a potentially underappreciated long-term ancillary play within the energy infrastructure space.

Disclaimer

This analysis is intended solely for informational purposes and does not constitute any investment or financial advice. All information is sourced from public company filings, analyst reports, and third-party sources believed to be reliable. In accordance with SEBI guidelines, market data is presented accordingly. Investors should conduct independent research, perform due diligence, and consult qualified financial advisors before making any investment decisions. The views expressed are personal and may be subject to errors or biases.