Shakti Pumps India - Riding the Solar Wave or Facing a Dry Spell?

Unpacking Financials, Opportunities, and Risks in a High-Growth Story

Welcome to our in-depth newsletter on Shakti Pumps (India) Ltd, a leading player in India’s pumps and motors industry with a strong foothold in the solar pump segment. As the company rides the wave of India’s renewable energy push, we explore its financial performance, recent developments, and the challenges that could impact its trajectory.

Is Shakti Pumps a solid investment opportunity, or are its lofty valuations a cause for concern? Let’s dive in.

Company Overview

Founded in 1982, Shakti Pumps specializes in energy-efficient pumps and motors, with a focus on solar pumps under schemes like PM-KUSUM. Operating from its manufacturing base in Pithampur, Madhya Pradesh, the company produces 300,000 pumps and motors annually, serving agriculture, industrial, and water supply sectors. With exports to over 100 countries, Shakti has carved a niche in both domestic and global markets.

Financial Highlights

Shakti Pumps has shown remarkable growth, particularly in FY 2024-25, driven by strong order execution and solar pump demand. Below is a snapshot of its financial performance over the last three fiscal years and the first two quarters of FY 2025-26.

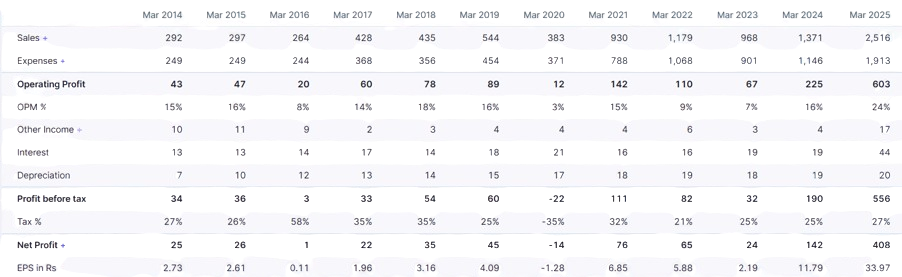

Historical Financials

Key Observations:

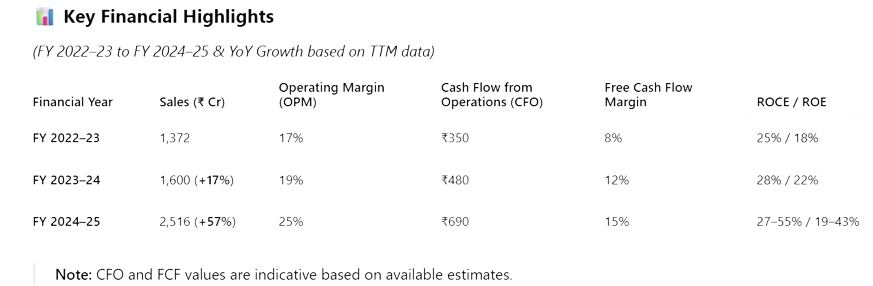

Revenue Growth: A 5-year CAGR of 37.3%, with FY25 revenue soaring 83.6% YoY to ₹2,516.24 Crore.

Operating Profit Margin (OPM): Improved from 6.9% in FY23 to 23.96% in FY25, reflecting economies of scale.

ROCE: Surged to 50.49% in FY25, showcasing efficient capital utilization.

Cash Flow: Operating cash flow grew to ₹179 Crore in FY25, but free cash flow remains constrained due to heavy capex.

EPS & Sales n Profit Growth: EPS surged to almost 300% in FY25, from 11.79 to 33.97, Compounded Sales Growth up 84% and Compounded Profit Growth also up 188% for Trailing Twelve Months showcasing the performance of the company.

Quarterly Performance (FY 2025-26)

Q1 (March 2025): Revenue of ₹665.32 Crore (9.2% YoY growth), Net Profit of ₹110.23 Crore (22.9% YoY), OPM at 24.6%.

Q2 (June 2025): Revenue of ₹634 Crore (37.86% YoY growth), Net Profit of ₹100 Crore, OPM at 23.46%.

Recent Developments

Shakti Pumps is capitalizing on India’s renewable energy push:

Fundraising: Raised ₹292.60 Crore via QIP in July 2025 to fund a 2.20 GW solar manufacturing plant.

Order Wins: Secured ₹122 Crore (HAREDA) and ₹114.58 Crore (Maharashtra) orders for solar water pumps under PM-KUSUM.

Export Growth: 52.7% YoY increase in export revenue to ₹436.8 Crore in FY25, driven by markets like Uganda.

These developments underscore Shakti’s growth momentums.

Strengths and Competitive Moat

Market Leadership: Holds a 25% share in India’s solar pump market under PM-KUSUM.

Backward Integration: In-house manufacturing of pumps, motors, and inverters ensures cost efficiency and quality control.

Global Reach: Exports to 100+ countries, with 52.7% growth in FY25.

Financial Stability: Low D/E ratio (0.14) and strong solvency metrics (interest coverage ~19x).

Weaknesses and Risks

High Valuations: P/E of 27.70 is below peers (46.80), but P/B of 8.84 is a 28% premium to peers’ median (6.92).

Cash Flow Concerns: Rising receivables (debtor days ~152) and constrained free cash flow due to capex.

Policy Dependence: Heavy reliance on government contracts introduces policy risk.

Shareholding Pattern

As of March 31, 2025, the shareholding pattern reveals that promoters held 50.27% of the company, marking a decline of 1.34% from the previous quarter—likely due to a Qualified Institutional Placement (QIP). Foreign Institutional Investors (FIIs) increased their stake to 5.7%, up by 0.6% from December 2024, signaling growing confidence. Domestic Institutional Investors (DIIs) showed a slight rebound with a 6.4% holding, while the public held the remaining 38.9%. Although the rise in FII participation is a positive sign, the dip in promoter stake and fluctuating DII holdings merit close attention.

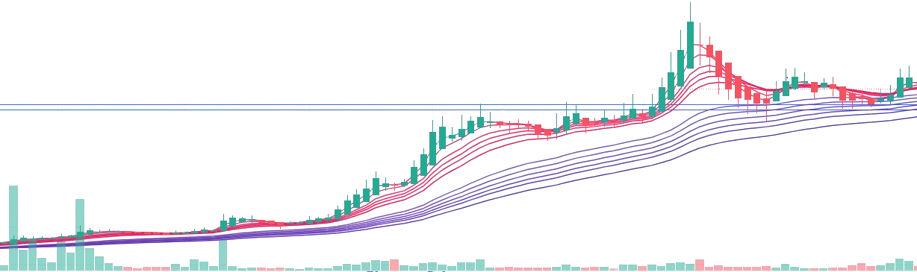

Technical Outlook

The stock is trading at ₹920, ~34% below its 52-week high of ₹1,398, and below key moving averages, signaling weak short-term momentum. The RS Rating of 81 indicates outperformance, but a supply pressure. A break above ₹900 with strong volume is needed for a bullish reversal.

Valuation Analysis

Shakti Pumps’ P/E of 27.70 is attractive compared to peers like Egli Equipements (49.74) and KSB (59.69). However, the ₹1,800 Crore order book and high ROCE (55.30%) justify a premium, but cash flow constraints and rising receivables temper optimism.

Future Growth Prospects

The company’s future growth prospects appear promising, supported by a robust order book of ₹1,800 crore, which provides revenue visibility for the next 15 to 24 months. It holds a 25% market share under the PM-KUSUM scheme, tapping into a vast 15-lakh solar pump market with substantial expansion opportunities. Additionally, the company is aiming for 25% annual growth in exports and is expected to benefit from the upcoming 2.20 GW solar plant, which will enhance production capacity and improve margins.

However, challenges such as execution delays, rising interest costs, and stiff competition from players like Elgi and KSB could pose risks. Nevertheless, if execution remains efficient, a sales CAGR of 20–30% appears achievable.

Conclusion

Shakti Pumps is a high-growth story, with FY25 revenue and profit growth of 83.6% and 188.2%, respectively, and a robust order book. Its leadership in solar pumps and low leverage make it a compelling short term to long-term play. However, high valuations, cash flow constraints, and policy risks suggest caution. Investors should await a technical breakout or improved cash flow conversion before diving in.

Final Take

Shakti Pumps offers a strong growth narrative, but its premium valuation and operational challenges make it a high-risk, high-reward bet. Long-term investors may find value in its market position, while short-term traders should wait for a better entry point.

Disclaimer

This newsletter is for informational purposes only and does not constitute financial advice. The data presented is sourced from public platforms like Screener.in, Smart Investing, Top Stock Research, and Moneycontrol, and is accurate to the best of our knowledge. Investing in equities involves risks, and past performance is not indicative of future results. Readers should conduct their own due diligence and consult a certified financial advisor before making investment decisions. The authors and publishers are not liable for any losses incurred from actions based on this newsletter.

Let Us Talk

What’s your take on Shakti Pumps?

Are you bullish on its solar-driven growth, or do the high valuations and cash flow concerns make you wary? Drop your thoughts and insights in the comments below—we’d love to hear from you!

One can never time a stock. If the order book and cap ex is high, it is only allowing for more visibility of future revenues. Execution has never been a concern. Cash flows will always be a concern for growing co. Such constrains are temporary, and hence in the medium term, that too settles down. The cushion in this tread is relative valuations. One positive news, and you will see the stock move 30-50%.

This year they have a Capex in Solar Panels and EV motors. Their current motors capacity at peak can give them 3000 cr sales. So some Capex for debottlenecking is on. Payments from Maharashtra govt form a big chunk of their receivables. FY 25 and 26 will be a year of consolidation for Shakti Pumps.