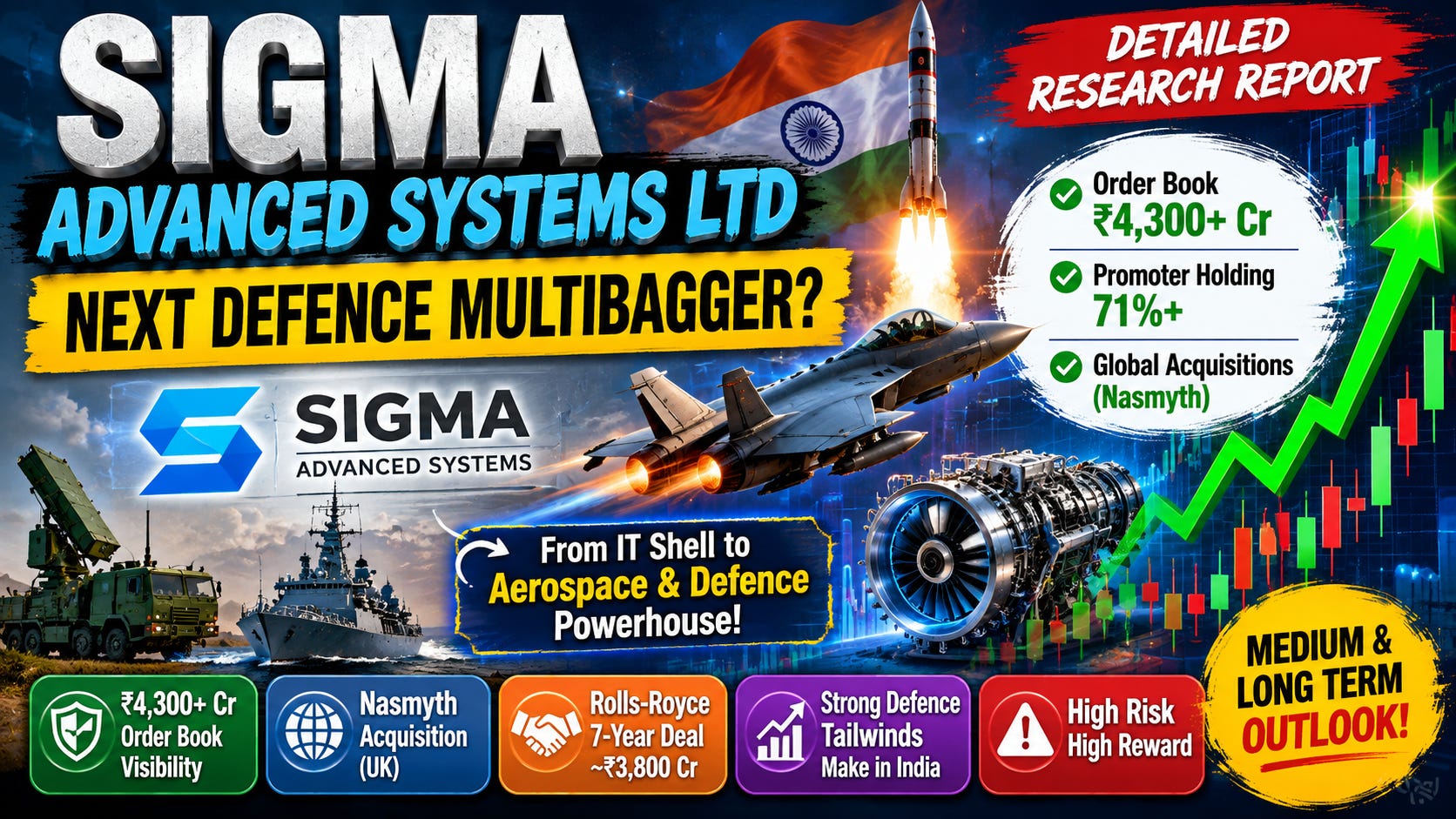

Sigma Advanced Systems - a Dormant IT Shell to an Emerging Aerospace & Defence Platform?

India’s Defence Story. Global Ambition. A High-Risk Aerospace Transformation with Multibagger Potential?

Sigma Advanced Systems has emerged as one of India’s notable aerospace and defence transformation stories. Formerly known as Megasoft Ltd, the company has reinvented itself from a small telecom and software business into a defence and aerospace manufacturing platform through mergers, acquisitions, and strategic restructuring.

The market now values Sigma as a potential global aerospace and defence player with UK aerospace exposure, Ministry of Defence relationships, and export-oriented growth opportunities. However, the story also comes with elevated valuations, low institutional participation, governance concerns, and high execution expectations.

The key question remains:

Can Sigma successfully evolve into a long-term aerospace & defence player, or has the market already priced in too much optimism?

Company Profile

Sigma is now positioned as an aerospace, defence electronics and precision engineering company with operations across India and the United Kingdom. The company focuses on avionics, missile systems, naval electronics, radar and counter-drone systems, precision actuation technologies, and aerospace manufacturing.

A major turning point came during FY26 when privately held Sigma Advanced Systems Pvt Ltd merged with the listed Megasoft entity through an NCLT-approved amalgamation. Following the restructuring, Chintalapati Holdings Pvt Ltd emerged as the dominant promoter, and the company was officially rebranded as Sigma Advanced Systems Ltd.

The restructuring effectively transformed the listed shell into a new aerospace and defence-focused manufacturing platform with global ambitions.

The Nasmyth Acquisition — The Defining Trigger

Sigma’s biggest transformation trigger came through the acquisition of UK-based aerospace engineering firm Nasmyth Group for nearly £1.8 million. The deal significantly strengthened Sigma’s global positioning as Nasmyth already had established relationships with aerospace giants such as Rolls-Royce, Airbus, Boeing, GE Aerospace, Safran, and Lockheed Martin.

The acquisition brought AS9100 aerospace certifications, advanced precision engineering capabilities and direct access to global aerospace supply chains. More importantly, it transformed Sigma from a small Indian defence player into an emerging international aerospace manufacturing platform — becoming one of the key reasons behind the stock’s sharp rerating.

The Rolls-Royce Opportunity

One of Sigma’s most significant developments was the reported long-term aerospace manufacturing agreement linked to Rolls-Royce programs, estimated at nearly ₹3,800 crore over seven years. For a company of Sigma’s historical scale, this represents a transformational opportunity.

Beyond revenue visibility, the deal carries strong strategic significance through validation from a global aerospace leader, improved credibility with international OEMs, long-term manufacturing visibility and potential participation in higher-value aerospace programs. If executed successfully, this partnership could become the foundation of Sigma’s long-term aerospace growth story.

Defence Orders & Revenue Visibility

Alongside its aerospace expansion, Sigma has significantly strengthened its defence electronics presence through multiple domestic and export orders. Recent inflows include over ₹100 crore in domestic defence contracts, nearly ₹315 crore of AS Strategic order visibility, and an USD 11.4 million artillery fuze export order from North America.

The company operates across strategic segments such as missile systems, naval electronics, avionics, SAM programs, anti-radiation missile electronics, and underwater platforms. Overall, Sigma currently has an estimated visible order and contract pipeline of nearly ₹4,300 crore spanning India, Europe, the United Kingdom, and North America.

This diversified order visibility across aerospace manufacturing, defence electronics, and export-oriented programs significantly strengthens the company’s long-term growth narrative and provides meaningful revenue visibility for the coming years.

However, a strong order book alone does not guarantee profitability — the real challenge now lies in execution, margin improvement and converting these opportunities into sustainable earnings and cash flows.

Promoter Restructuring & Holding Surge

One of the most discussed developments in Sigma’s transformation has been the sharp rise in promoter holding from nearly 35% to over 71%. This increase occurred through the NCLT-approved amalgamation scheme, under which new shares were allotted and Chintalapati Holdings Pvt Ltd emerged as the dominant promoter entity.

The change was not a conventional open-market acquisition but part of a broader reverse-merger restructuring that significantly expanded the company’s equity base, leading to dilution for existing public shareholders. While the higher promoter stake reflects strong long-term commitment and control, it also brings increased focus on governance standards, minority shareholder protection, and long-term capital allocation discipline.

Financial Position & Valuation Analysis

Sigma’s current valuation is driven more by future growth expectations than by its present earnings profile. The market is largely pricing the company as an emerging aerospace and defence platform with significant long-term scaling potential rather than valuing it on traditional near-term fundamentals. Investor optimism is centered around:

the Nasmyth integration,

the Rolls-Royce-linked opportunity,

expanding defence order visibility,

possibility of Sigma evolving into a much larger global aerospace and defence manufacturing player over the next 3–5 years.

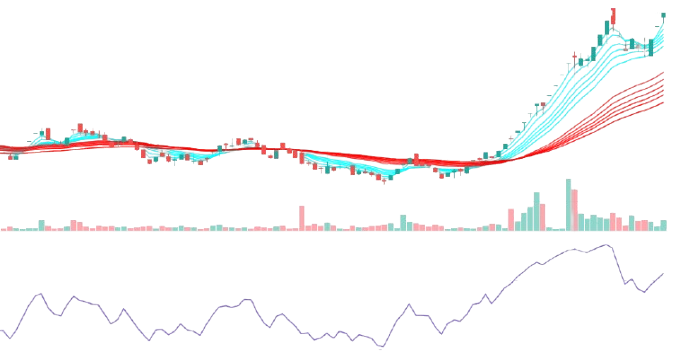

Technical Chart Analysis

Based on the attached daily chart, the technical structure remains strongly bullish.

The chart structure reflects a strong bullish trend, highlighted by a decisive breakout from a prolonged consolidation phase, supported by expanding GMMA alignment, sustained price momentum, and rising trading volumes that confirm strong market participation. The stock is also trading comfortably above all major moving averages, indicating healthy trend continuation and sustained bullish strength in the broader structure.

The RSI near 74 indicates strong bullish momentum and sustained buying interest, although it also suggests that the stock may be approaching near-term overbought levels, making short-term volatility or profit booking possible.

Technically, the ₹308–322 zone is expected to act as an important immediate support area, while ₹355–360 remains near-term resistance range. A decisive breakout above recent highs could potentially trigger the next momentum, although sharp volatility and periodic profit booking are likely to remain part of the stock’s broader trading structure.

Why Sigma Can Be Considered for Medium-Term Investment

Sigma’s medium-term growth potential depends on the successful execution of its aerospace and defence transformation. Key triggers over the next 1–3 years include smooth Nasmyth integration, improving revenues and margins, repeat defence orders, and scaling aerospace manufacturing operations.

If execution remains strong, the company could witness meaningful growth, improving valuations and rising institutional interest. The broader defence sector also continues to benefit from India’s indigenisation push, increasing defence exports, rising geopolitical spending, and growing global aerospace outsourcing opportunities — trends that Sigma is strategically positioning itself to capitalize on.

Long-Term Investment Outlook

Sigma’s long-term story lies in its attempt to build a rare India-listed aerospace and defence platform with global manufacturing integration. Its India–UK structure combines cost-efficient Indian manufacturing with UK aerospace certifications, export credibility, and access to global OEM supply chains.

If execution remains strong over the next 5–7 years, Sigma could evolve into a meaningful aerospace and defence manufacturing player. The opportunity is further supported by rising global defence spending, European rearmament, NATO expansion, Indo-Pacific tensions and defence supply-chain diversification.

With exposure across aerospace precision engineering, missile systems, avionics, naval electronics, and ammunition systems, Sigma is positioned within some of the fastest-growing defence segments globally.

Key Risks & Negatives

Despite the strong growth narrative, Sigma continues to face significant risks, with execution remaining the biggest concern. The company must simultaneously manage international integration, aerospace manufacturing scale-up, defence program execution, governance stabilization, and margin improvement.

Other key risks include low institutional participation, ASM surveillance status, governance concerns, volatility due to limited public float, FX exposure from UK operations and elevated valuations that leave little margin for execution errors or delays.

Conclusion & Final Take

Sigma is no longer a legacy IT company. Through its reverse-merger transformation, UK aerospace acquisition, global OEM integration and defence electronics expansion, the company has repositioned itself as an ambitious aerospace and defence manufacturing platform with global aspirations.

The company now benefits from strong order visibility, expanding aerospace access, improving defence sector positioning and aggressive promoter intent. However, elevated valuations, governance concerns, and execution challenges remain important risks that investors cannot ignore.

For investors with a high-risk appetite, long-term patience and conviction in India’s aerospace and defence manufacturing opportunity, Sigma could emerge as a rewarding transformation story. However, the next few quarters will be crucial, as the market now expects strong execution and sustained financial delivery — not just future promises.

Disclaimer: This analysis is intended solely for informational purposes and does not constitute any investment or financial advice. All information is sourced from public company filings, analyst reports, and third-party sources believed to be reliable. In accordance with SEBI guidelines, market data is presented accordingly. Investors should conduct independent research, perform due diligence, and consult qualified financial advisors before making any investment decisions. The views expressed are personal and may be subject to errors or biases.

Let Us Talk

What is your view on Sigma Advanced Systems Ltd? Share your thoughts, targets, concerns, and perspectives.