Spandana Sphoorty Financial Ltd — From the Ashes to the Ascent

A Battered MFI Giant Rebuilding from the Ground Up. Is the Darkest Hour Finally Behind Us?

Spandana Sphoorty Financial, incorporated in 2003 and listed in 2019, is among India’s larger NBFC-MFIs focused on rural and semi-urban borrowers, primarily women under the Joint Liability Group model and operates across 20 states/UTs.

The company survived the Andhra Pradesh MFI crisis (2010–11), underwent CDR restructuring, and delivered strong growth post-2017. It is currently navigating another sector stress cycle in FY25–FY26.

Though it is a loss making NBFC but still to discuss and study what Has Been Happening at Spandana?

FY25–FY26 witnessed sector-wide stress due to borrower over-leverage and aggressive prior disbursement growth.

Q3 FY26 Snapshot

Standalone net loss: ₹82–95 Cr (vs ₹249 Cr in Q2)

PPOP: ₹8 Cr (vs -₹40 Cr in Q2)

Technical write-offs (9M FY26): ₹1,155 Cr and Q3 write-offs: ₹207–214 Cr

GNPA (Standalone): 2.6% (down from 4.97%) and NNPA: 0.5–0.9%

Aggressive write-offs indicate front-loaded balance sheet cleansing.

Disbursement Momentum

Q1 FY26: ₹280 Cr

Q2 FY26: ₹934 Cr

Q3 FY26: ₹1,188 Cr (+27% QoQ)

Collection Efficiency

New book (post-April 2025): ~99.8%

New book now ~58% of AUM; expected ~90% by FY26-end

The recovery in collections and new disbursements signals stabilization.

1️⃣ Financial & Balance Sheet Highlights (FY25)

Capital Adequacy

CRAR (Mar 2025): 36.31%

Post-rights CRAR: ~47% - Entirely Tier I capital

Liquidity Position

₹1,179 Cr (Sept FY26)

₹1,270 Cr (Oct FY26)

₹1,506 Cr (Q3 buffer)

~25% liquidity to total assets

Debt Reduction

FY24: ₹9,012 Cr

FY25: ₹5,197 Cr

Sept 2025: ~₹3,072 Cr

FY25 financing outflow: ₹3,761 Cr

Operating Cash Flow

FY25 CFO: ₹3,783 Cr

This swing confirms collections are generating real cash and liquidity stress risk is low.

The Real Story in the Numbers is in Cash Flow, Deleveraging & Book Value

Earnings remain volatile due to provisioning, but cash flow reveals operational stability. The ₹3,783 Cr operating cash flow in FY25 confirms the core business viability; Strong collections; Reduced refinancing risk simultaneously, deleveraging improves future ROE potential.

Book Value & Valuation

Book Value per Share: ~₹293

CMP: ₹253

Historically, MFIs trade at 1.5–2.5x book during normalized cycles. Current valuation reflects continued stress pricing.

Deferred Tax Asset: The company holds a Deferred Tax Asset of approx ₹643–700 crore, which is expected to be utilized over the next eight years. The recognition of this DTA indicates management’s confidence in the company’s profitability recovery and its ability to generate sufficient taxable income in the coming years to absorb these tax benefits.

The Turning Point Thesis

The Worst Seems Over — Already reflected in the Price

Stock corrected ~65–70% from peak and market seems has absorbed:

Six quarters of losses

~57% revenue contraction

₹1,155 Cr write-offs

AUM contraction

Technical write-offs accelerate cleanup and improve forward visibility.

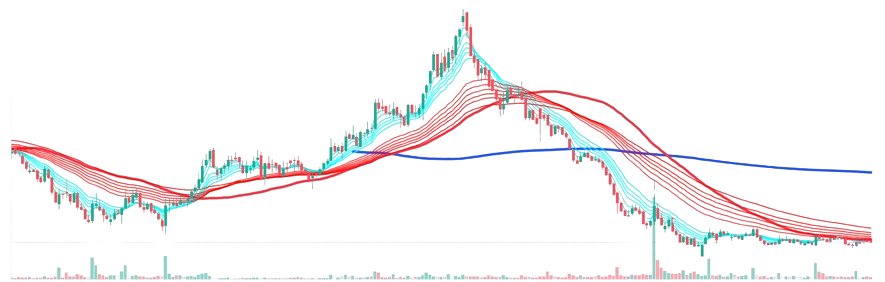

Technical Chart Analysis — Daily Timeframe

10+ month consolidation between ₹183–320

GMMA compression indicating trend transition

200 DMA ~₹263 near current price

Higher-low formation at ₹183

Extended consolidation typically precedes structural moves.

With the following assumptions, the company may offer the handful appreciation in near future:

Credit cost normalization: 2.5–3%

AUM growth to ₹9,000–10,000 Cr by FY28

NIM stabilization ~11%+

Break-even by Q4 FY26

Future Growth Expectations and Why the Recovery Story is Credible

India’s rural credit gap remains structurally large, which provides a long-term opportunity for well-established microfinance players. The recovery story of Spandana appears credible as the company benefits from over 20 years of operating experience, a deep and well-penetrated rural network, a strong capital buffer, and a cleaned-up loan book following recent stress. In addition, ongoing management transformation initiatives are aimed at strengthening risk controls and improving operational efficiency. The new loan book’s collection efficiency of over 99% further confirms the company’s operational resilience and execution strength.

Conclusion & Final Take

The Darkest Night Precedes the Brightest Dawn

Spandana’s investment thesis rests on three pillars:

Strong operating cash flows

Active deleveraging

Valuation near book value

While earnings remain volatile, balance sheet risk has reduced significantly. If management achieves break-even in Q4 FY26 and sustains disciplined growth, re-rating potential is meaningful.

Turnarounds demand patience — but when supported by cash flow, capital strength, and cleanup execution, they can offer asymmetric long-term returns.

Disclaimer

This analysis is intended solely for informational purposes and does not constitute any investment or financial advice. All information is sourced from public company filings, analyst reports, and third-party sources believed to be reliable. In accordance with SEBI guidelines, market data is presented accordingly. Investors should conduct independent research, perform due diligence, and consult qualified financial advisors before making any investment decisions. The views expressed are personal and may be subject to errors or biases.

Let us talk

What are your thoughts on Spandana’s outlook? Have questions or different views on the targets? Let us know in the comments below – we’d love to hear from fellow investors!