Syrma SGS Technology _ a Record-Breaking Performance

A Year of Growth, Innovation, Strategic Expansions, and a Bold Vision for FY 2025

Company Overview

Syrma SGS Technology is a prominent Indian electronics manufacturing services (EMS) provider, specializing in high-mix, flexible volume production. The company serves diverse sectors, including automotive, telecom, industrial, IT, consumer electronics, railways, healthcare, and defense. Over the years, Syrma SGS has established itself as a key player in the EMS industry, leveraging its design-focused approach and extensive domain knowledge.

Financial Performance: FY 2023-24

• Revenue from Operations: ₹3,170.68 crore

• Net Profit After Tax: ₹124.34 crore

• Net Profit Margin: 3.94% (down from 6.01% in the previous year)

• Debt-to-Equity Ratio: 0.05 (down from 0.09 in the previous year)

• Return on Equity (ROE): 7.72%

Significant Updates

• Acquired a 51% stake in Johari Digital Healthcare Limited, expanding into medical equipment manufacturing.

• Revenue growth driven by higher sales in electronics manufacturing and entry into the medical equipment sector.

• Margins impacted by rising raw material costs and competitive pricing pressures.

Financial Performance: Q1 & Q2 FY 2025

• Q1 Revenue: INR 1,134 crore, growing 67% YoY.

• Q2 Revenue: INR 834 crore, a 17% YoY increase.

• EBITDA Growth: Operating EBITDA for Q2 FY 2025 was 8.8%, reflecting strong improvement.

• Order Book Strength: Current order book stands at INR 4,800 crore, with sustained growth in the auto, industrial, consumer, and healthcare segments.

• Operational Cash Flow: Recorded INR 211 crore in H1 FY 2025, driven by improved working capital efficiency.

Recent Developments

• Commissioned a new manufacturing facility in Pune, further enhancing production capacity.

• Received PLI approval for the MedTech business, enabling expansion in the healthcare sector.

• Onboarded 9 new clients in H1 FY 2025, with an expected revenue potential of over INR 500 crore.

• Expanded into Germany with a 40,000 sq. ft. facility to meet European near-shoring demands.

• Launched a new IoT and RFID-based product line, diversifying our offerings in connected devices.

Challenges Faced

• Decline in gross margin due to increased reliance on the lower-margin consumer electronics segment.

• Ongoing working capital pressure, despite efforts to shorten cycle times.

• Delays in export orders due to market slowdowns in Europe and the USA.

• High dependency on imported raw materials, exposing the company to forex risks.

SWOT Analysis

Strengths:

• Strong R&D capabilities and innovation-driven approach.

• Expanding global footprint with significant export growth.

Weaknesses:

• Working capital-intensive operations.

• Dependence on the consumer segment for revenue stability.

Opportunities:

• Expansion in smart metering, RFID, and MedTech ODM sectors.

• Government incentives via PLI approvals in healthcare devices.

• Rising global demand for EMS solutions.

Threats:

• Forex risks due to high import dependency.

• Increased competition in the EMS sector.

Technical Outlook

• AI & Robotics Integration: Automation to enhance efficiency and cost management.

• IoT & Smart Electronics: Strengthening our position in connected devices.

• ODM Expansion: Growth in high-margin ODM offerings to boost profitability.

Valuation Justification

Syrma SGS Technology’s valuation is supported by strong fundamentals, including:

• Consistent revenue and profit growth, with a 33.51% CAGR over the past three years.

• Diversified revenue streams across industries, reducing risk exposure.

• Robust order book ensuring steady cash flow and future revenue growth.

• Significant investments in innovation and capacity expansion for long-term value creation.

• PLI incentives and government support providing additional financial stability.

These factors support Syrma SGS’s current valuation and highlight the potential for future growth.

Future Outlook & Market Strategy

• Revenue Growth Target: Aiming for 40-45% growth in FY 2025, driven by demand across automotive, electric mobility, industrial, RFID, and healthcare sectors.

• Consumer Segment: Expected to stabilize at 37-40% of total revenue.

• Export Growth: Despite potential softness in H1 FY 2025, exports are projected to grow by 30%.

• EBITDA Margins: Expected to stabilize at 7% annually, with quarterly variations based on demand.

• Financial Strength: The company remains OCF-positive with a consistent dividend payout of 15%, in line with last year.

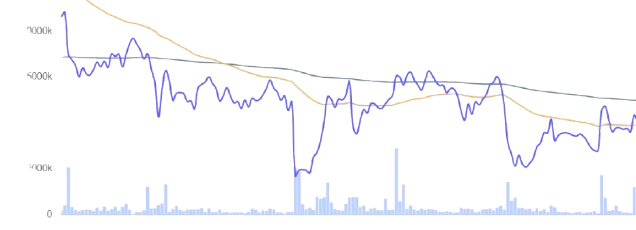

Chart, Base formation and Conclusion

Syrma SGS Technology continues to demonstrate leadership in innovation, growth, and financial resilience. With strategic expansions, a strong order pipeline, and ongoing investments in advanced technology, the company is well-positioned for sustained success in FY 2025 and beyond. Its robust technical capabilities and global outreach remain key drivers of long-term value creation.

Given its strong performance and forward-looking strategies, expanding manufacturing capabilities, a commitment to innovation, and strong customer partnerships, the company is well-equipped to seize emerging opportunities in the electronics manufacturing sector. Investors and stakeholders are encouraged to closely monitor its progress, as its growth trajectory and technological advancements signal substantial long-term potential.

Disclaimer: This analysis is for educational and informational purposes only and does not constitute any financial advice. In its latest circular, SEBI has clarified that individuals providing stock market education must use stock price data with a three-month lag. Accordingly, all data and charts presented here comply with these guidelines. Investors should conduct their own due diligence before making any investment decisions. The author being invested in the company, opinions expressed are personal, potentially biased, and may contain inaccuracies. Additionally, all figures are subject to verification.

Indeed it is looking great from long term perspective. In my watchlist for a while, thanks for detailed write-up.