Tata Motors Passenger Vehicles Ltd (TMPV)

A Post-Demerger Auto Giant at an Inflection Point? Financials Improving, Technicals Stabilising - CMP: ₹337.95 | NSE | Daily Chart Analysis

Since its listing following the Tata Motors demerger, TMPV has experienced a significant correction, largely driven by concerns surrounding Jaguar Land Rover, weaker global luxury vehicle demand and temporary operational disruptions. However, the latest quarterly results suggest that the worst may be behind the company.

While the stock is yet to confirm a fresh uptrend technically, improving operating performance and an attractive valuation make it an interesting candidate for investors willing to accumulate during periods of weakness.

Demerger Benefits

The demerger has created a focused passenger vehicle company comprising:

Tata Passenger Vehicles

Tata EV business

Jaguar Land Rover (JLR)

The key advantages include:

Independent management focus

Better capital allocation

Transparent financial reporting

Separate valuation from the commercial vehicle business

Greater flexibility for strategic partnerships and future fund raising

These structural benefits are expected to unlock shareholder value over time.

Quarterly Financial Performance

TMPV’s consolidated financial performance over the last three quarters reflects a clear turnaround in business momentum. Revenue stood at ₹72,349 crore in the September 2025 quarter before moderating slightly to ₹70,108 crore in December 2025, as the company continued to grapple with the impact of the JLR cyberattack, subdued demand in the Chinese market, and temporary production disruptions. However, the March 2026 quarter marked a remarkable recovery, with revenue surging to ₹105,447 crore, representing a quarter-on-quarter growth of more than 50%. This sharp rebound indicates that operational challenges have largely eased, demand has strengthened, and the company has regained significant business momentum, providing encouraging signs for investors regarding the sustainability of its recovery.

Operating Profit

TMPV’s operating performance over the past three quarters highlights a significant turnaround in profitability. The company reported an operating loss of ₹1,404 crore in the September 2025 quarter, resulting in an Operating Profit Margin (OPM) of -2%, reflecting the adverse impact of the JLR cyberattack, weak global demand and production disruptions. The situation improved in the December 2025 quarter, with the company returning to an operating profit of ₹879 crore and a modest OPM of 1%, signalling the beginning of a recovery. The turnaround gained substantial momentum in the March 2026 quarter, when operating profit surged to ₹11,259 crore, accompanied by a healthy OPM of 11%. This sharp sequential improvement demonstrates that the company has largely overcome the temporary operational challenges, restored profitability and significantly strengthen its operating efficiency. If this trend continues over the coming quarters, it could pave the way for improved earnings quality and enhanced investor confidence. Source: Screener.in

Valuation

One of the most striking features of TMPV is its valuation.

Current P/E: 1.44

At first glance, this appears extraordinarily cheap. However, investors should interpret this figure with caution because it is heavily influenced by one-time accounting gains arising from the demerger, which temporarily inflated reported earnings. As these exceptional items roll off, the P/E is likely to normalize.

Even after allowing for these accounting effects, TMPV continues to trade at a valuation discount compared with major listed passenger vehicle peers, reflecting investor caution over JLR and global demand. If operating performance continues to recover, this discount has the potential to narrow over time.

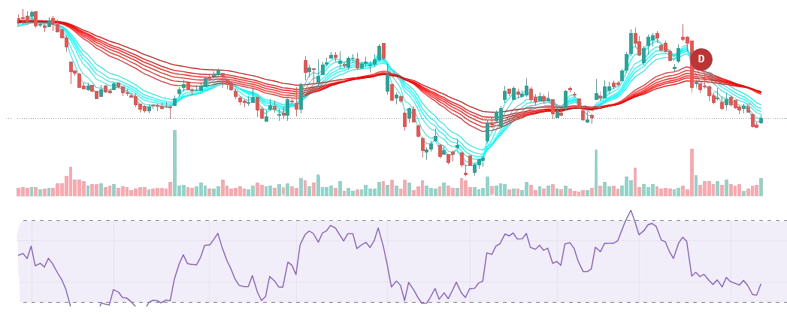

Technical Analysis

Price Action

The daily chart indicates:

Approximately 20% correction from recent highs.

Price has started stabilising around ₹330–335.

Selling pressure has reduced significantly.

Early signs of a base formation are emerging.

GMMA Analysis

The moving average ribbon shows:

Short-term averages are beginning to compress.

Price is attempting to reclaim the faster moving averages.

This suggests the stock is transitioning from a downtrend toward a potential accumulation phase, although confirmation is still awaited.

RSI Analysis

Current RSI: 38.70

Interpretation:

The stock is no longer deeply oversold.

Downside momentum has weakened.

RSI is attempting to turn upward.

A move above 50 would provide stronger confirmation of renewed buying momentum.

Relative Strength

Relative Strength versus the broader market remains marginally negative, indicating that the stock has underperformed in recent months.

However, the RS line has flattened, suggesting that underperformance is reducing. An improvement above the zero line would be an encouraging sign of renewed institutional participation.

Strengths

Tata Group pedigree.

Strong domestic passenger vehicle franchise.

Market leadership in electric passenger vehicles.

Global presence through Jaguar Land Rover.

Significant operating turnaround in the latest quarter.

Benefits expected from the demerged corporate structure.

Key Risks

Dependence on JLR profitability.

Global luxury vehicle demand remains uncertain.

China market weakness.

Intense competition in the passenger vehicle segment.

Investment Outlook: Short-Term

The technical structure suggests the stock is attempting to establish a bottom. A decisive breakout above the ₹350–355 resistance zone, supported by stronger volumes and improving Relative Strength, could trigger the next upward move.

Investment Outlook: Medium-Term

If the company continues to report improving quarterly revenues and operating margins while JLR maintains its recovery trajectory, investor confidence is likely to improve.

EXPECTED A MEANINGFUL APPRECIATION POTENTIAL

This upside would be supported by:

Continued earnings recovery.

Margin normalisation.

Improvement in Relative Strength.

Potential valuation re-rating as one-off demerger effects fade and the market focuses on underlying operational performance.

Recurring Volume Pattern: Is History Beginning to Repeat?

One interesting observation from the daily chart—though not based on any formal investment or charting strategy—is the recurring relationship between volume spikes, RSI behaviour and subsequent price appreciation.

In each of the previous rallies, a noticeable increase in trading volumes appeared just before a meaningful upward move in the stock price. Around 19–20 December 2025, a sharp rise in volume was followed by an advance from approximately ₹346 to ₹374. A similar pattern emerged during 2–3 February 2026, when renewed buying interest preceded a rally from around ₹343 to ₹391. Again, in the first week of April 2026, increasing volumes coincided with the stock recovering from nearly ₹309 to ₹363, before extending its move to approximately ₹401–402.

Interestingly, the current chart is once again showing early signs of increasing trading volumes, while the RSI is hovering around levels similar to those seen before the earlier rallies. Although this observation alone is insufficient to form an investment decision or trading strategy, it does raise an intriguing question:

Could TMPV be entering another accumulation phase similar to those witnessed in the past?

If history were to repeat itself, and if improving volumes are accompanied by a breakout above key resistance levels with strengthening Relative Strength (RS), the stock could potentially embark on another meaningful upward move. However, investors should treat this as an observational pattern rather than a predictive signal, and wait for price confirmation before drawing any bullish conclusions.

Conclusion

TMPV appears to be moving through the final stages of a post-demerger adjustment. The latest quarter has demonstrated a sharp turnaround in both revenue and operating profitability, while the technical indicators suggest that downside momentum is fading.

Although the trend has not yet turned decisively bullish, the combination of improving fundamentals, stabilising price action and an attractive valuation profile makes the stock worth monitoring closely.

For investors with a medium-term perspective, gradual accumulation on declines may offer a favourable risk-reward proposition, provided the stock confirms strength above key resistance levels.

Disclaimer

This report is intended solely for educational and informational purposes and should not be construed as investment advice or a recommendation to buy or sell any security. Financial data has been sourced from publicly available information on Screener.in and other publicly available reports, while the technical analysis is based on the charts provided by the user. The reported P/E ratio is influenced by demerger-related accounting adjustments and should be interpreted with caution. Investors should conduct their own due diligence and consult a SEBI-registered investment advisor before making investment decisions.