Wendt India - A Diamond in the Rough or Losing Its Edge?

Evaluating the Challenges Facing a Precision Engineering Leader

🔍 Executive Summary

Wendt India, a pioneer in super abrasives and precision engineering, stands at a strategic inflection point. Despite its strong pedigree, robust R&D, and a debt-free balance sheet, the recent full exit by German promoter Wendt GmbH, coupled with margin pressures and stock underperformance, has cast a shadow over its outlook. This edition provides a comprehensive analysis of the company’s financials, key developments, and strategic positioning.

🏢 Company Snapshot

Wendt India, founded in 1980, is a joint venture between Wendt GmbH (a subsidiary of the Carl Zeiss Group, Germany) and Carborundum Universal Ltd of the Murugappa Group. The company operates across three primary business segments: Super Abrasives, which contribute 59% of revenue; Machines and Accessories, accounting for 21%; and Precision Products, which comprise the remaining 12%. With a strong global footprint, Wendt India exports its products to over 40 countries, serving key industries such as automotive, aerospace, steel, and ceramics.

🚨 Key Development: Wendt GmbH’s Exit via OFS

In May 2025, Wendt GmbH divested its entire 37.5% stake in Wendt India through an Offer for Sale at a floor price of ₹6,500 per share, representing a steep 38% discount to the prevailing market price. The announcement led to a sharp 17% decline in the company’s stock, sparking investor concerns over strategic continuity and leadership stability. The OFS was well-received, with strong institutional demand leading to a subscription rate of 436%. The total offer size stood at ₹487 crore. Following the sale, Wendt GmbH exited completely, leaving Carborundum Universal (CUMI) as the sole promoter with a 37.5% stake.

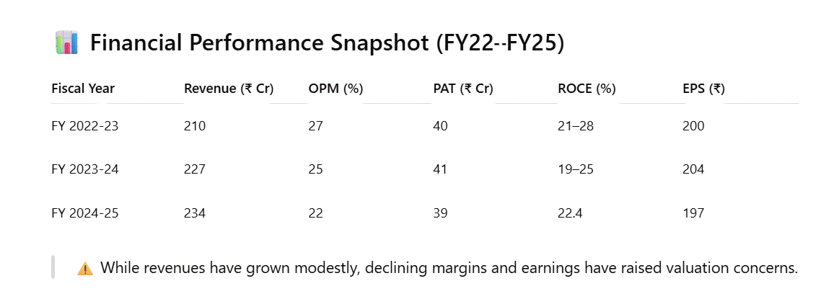

📊 Financial Performance Snapshot (FY22–FY25)

🧩 Strategic Challenges & Risks

Promoter Exit: Wendt GmbH’s departure brings strategic and governance uncertainties.

Export Headwinds: Global slowdown and increasing competition from Chinese players.

Innovation Imperative: Pressure to deliver returns on new launches like the WXG 750 and OPRA 400 series.

🛡 Competitive Edge

✅ In-house R&D: Backed by years of innovation and precision engineering

✅ Niche Leadership: Dominant player in super abrasives with limited competition

✅ Strong Brand Equity: Established global reputation across industrial sectors

⚠️ Competitive Threats: Growing pressure from global majors (e.g., 3M) and local players (e.g., Roto Pumps)

📈 Valuation Overview

As of the latest available data, Wendt India is trading at a PE ratio of 43.00x and a PEG ratio of 1.25x, indicating a premium valuation relative to industry norms, while the ROCE is a healthy 22.40%. Its market capitalization is approximately ₹1,700 crore. Despite strong returns, the valuation appears stretched when compared to its recent earnings trajectory. A more reasonable PE band of 30–35x would better reflect the company’s current fundamentals and profit growth potential.

🧮 SWOT Analysis

Strengths

Wendt India benefits from a debt-free balance sheet, enabling financial flexibility and stability. Its strong in-house R&D capabilities, backed by decades of precision engineering experience, give it a technological edge in the niche market of super abrasives. The company also enjoys access to global markets, exporting to over 40 countries, which diversifies its revenue base and enhances its brand reputation internationally.

Weaknesses

Despite its strengths, the company faces operational challenges, including rising debtor days, which increased to 107 in FY25—suggesting inefficiencies in working capital management. Additionally, margin compression due to input cost inflation and limited operating leverage has impacted profitability. Its premium valuation, with a PE ratio exceeding 43x, appears stretched given the recent slowdown in earnings growth.

Opportunities

Wendt India is well-positioned to capitalize on emerging sectors such as aerospace, electric vehicles (EVs), and renewable energy. These industries demand high-precision components—an area where Wendt excels. Furthermore, the company has room to expand exports to underserved regions like West Asia and Southeast Asia. Continued innovation, especially with new machine series like the WXG 750 and OPRA 400, also presents growth avenues.

Threats

The recent exit of promoter Wendt GmbH raises concerns around strategic continuity and corporate governance. Global recessionary trends and a slowdown in industrial activity pose macroeconomic threats. Additionally, competition from low-cost Chinese and domestic manufacturers could erode market share and exert pricing pressure. Rising raw material costs further challenge margins, particularly in a business that relies heavily on imported inputs.

🎯 Investor Verdict: Cautious Optimism

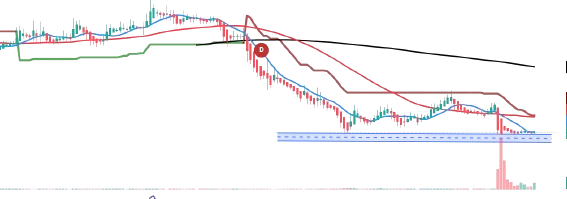

** Wendt on Daily Chart

The price has been corrected from the ATH of ₹18,034/- to the current levels of ₹8,500/- and the stock seems consolidating in the Accumulation Phase and a reversal to the Uptrend Phase can give the investing opportunity.

Key Triggers to Watch:

Q4 FY25 earnings

Order inflows for new machines

Margin trends post-promoter exit

📌 Investors are advised to wait for earnings recovery and a clearer strategic roadmap before increasing exposure.

⚠️ Disclaimer

This analysis is for educational and informational purposes only and does not constitute financial advice. All data is sourced from public company filings, analyst reports, and third-party sources believed to be reliable. In line with SEBI’s guidelines, all market data is presented with a three-month lag. Investors should carry out their own due diligence and consult the financial advisor before making any investment decisions. The views expressed are personal and may be subject to errors or bias.

💬 Community Corner

We’d love to hear your views:

Is Wendt India's margin pressure temporary or structural?

Will the company’s export engine restart in FY26?

Does Wendt GmbH’s exit mark an opportunity or a red flag?

Would you invest at current levels?

Share your insights with us! 💬📢