When Sky-High Valuations Meet Ground-Level Concerns – ZEN TECHNOLOGIES - Defence Tech Giant at a CROSSROADS

A Deep Dive into India's Defence Simulation Giant

📊 EXECUTIVE SUMMARY

Zen Technologies Limited stands as India's foremost defence simulation company yet finds itself navigating turbulent waters in 2025. While the company boasts impressive fundamentals—including a ₹1,402 crore order book and debt-free status—recent financial volatility and stretched valuations demand careful investor scrutiny.

Key Investment Thesis: Strong fundamentals meet valuation reality check.

🏢 COMPANY SNAPSHOT

Business Profile: Zen Technologies specializes in combat training simulators, anti-drone systems, and driver training solutions, serving defence and civilian markets globally.

Market Position:

India's largest supplier of simulation training equipment

1,000+ training systems shipped globally

54 patents in defence technology

Strategic presence across Asia, Europe, and expanding into the US market

📈 FINANCIAL PERFORMANCE ANALYSIS FOR PAST 3 YEARS

FY 2022-23: The Breakout Year

Revenue: ₹218.85 Cr (+213.7% YoY)

Net Profit: ₹49.97 Cr (+1,814% YoY)

Operating Margin: 34.1%

FY 2023-24: Growth Acceleration

Revenue: ₹439.85 Cr (+101.0% YoY)

Net Profit: ₹129.50 Cr (+159.2% YoY)

Operating Margin: 41.6% (Peak performance)

FY 2024-25: Scale-Up Challenges

Revenue: ₹973.64 Cr (+121.4% YoY)

Net Profit: ₹299.38 Cr (+119.1% YoY)

Operating Margin: 28.89% (Margin compression)

🔍 COMPETITIVE MOAT & SWOT ANALYSIS

🏰 MOAT FACTORS (Competitive Advantages)

Technology Leadership: 54 patents including cutting-edge laser-based combat training systems

Market Dominance: Largest player in India's defence simulation market

Global Footprint: Export presence in Europe, UAE, and expanding US operations

Financial Fortress: Debt-free with ₹1,028 crore cash reserves

✅ STRENGTHS

Revenue Growth: 31.70% CAGR over five years

Order Book Visibility: ₹1,402 crore provides revenue certainty

Innovation Pipeline: Continuous R&D investment and patent development

Strategic Acquisitions: Recent TISA Aerospace acquisition (₹6.60 Cr) for UAV capabilities

⚠️ WEAKNESSES & CONCERNS

Profit Volatility: 40.80% QoQ decline in Q3 FY26 raises execution concerns

Working Capital Strain: 154 debtor days impacting ROCE and cash conversion

Valuation Premium: P/E of 61.15 (33% above peer median of 45.78)

Margin Pressure: Operating margins declined from 41.6% to 28.89%

📊 VALUATION DEEP DIVE

Company is currently trading at a P/E ratio of 61.15 and a P/B ratio of 9.87, which is higher than the peer median of 6.28—placing it firmly in premium valuation territory. The PEG ratio stands at 1.71, reflecting optimism around growth. This premium is supported by a strong order book, government spending in the defence sector, and growing export opportunities. However, concerns remain due to high valuation multiples amid margin pressures and recent profit volatility, which also raise execution risk flags.

🚀 GROWTH CATALYSTS & FUTURE OUTLOOK

Key Growth Drivers

Defence Modernization: India's ₹6.81 lakh crore defence budget supports sector growth

International Expansion: US market entry through AVT Simulation partnership

Technology Evolution: Entry into loitering munitions and UAV segments via TISA acquisition

Infrastructure Development: New R&D facility in Goa enhancing production capacity

Revenue Projections

Analyst Consensus: 20-25% revenue CAGR over next 3-5 years

FY26 Guidance: Based on current order book execution

Export Target: Significant contribution from international markets

📉 RISK FACTORS & RED FLAGS

Recent Warning Signs

Stock Performance: 31.08% YTD decline despite strong fundamentals

Foreign Investor Exodus: FII holdings decreased from 8.29% to 5.95%

Execution Concerns: Order book conversion challenges

Key Risks to Monitor

Lumpy Revenue: Defence contracts create quarterly volatility

Competition: Increasing players in defence technology space

Regulatory Changes: Government policy shifts affecting defence spending

Technology Obsolescence: Rapid evolution requiring continuous R&D investment

📊 SHAREHOLDING PATTERN ANALYSIS

Shareholding pattern reveals key shifts in investor sentiment and strategic positioning. Promoters continue to hold a dominant 49.05% stake, though this reflects a stable yet gradually declining trend—likely driven by the company’s need to raise growth capital. FII have reduced their stake from 8.29% to 5.95%, signaling a degree of caution, on the other hand, DII have increased their holding to 9.47%, highlighting growing confidence among local institutions, particularly in the resilience and potential of the defence sector. These dynamics underline a shift in investor composition, with domestic institutions stepping up as foreign investors take a more cautious stance.

** Zen Technologies Limited (ZENTEC.NS) Analyst Ratings, Estimates & Forecasts - Yahoo Finance

🎯 INVESTMENT RECOMMENDATION

Zen Technologies presents a compelling long-term story built on India's defence modernization and export potential. However, current valuations appear stretched relative to near-term fundamentals.

Target Investor Profile

Long-term Growth Investors: Strong secular trends support multi-year growth

Thematic Play: Pure-play exposure to defence technology megatrend

Risk Tolerance: High, given volatility and execution risks

Entry Strategy

Gradual Accumulation: Build positions during market corrections

Price Targets: Consider entry on every correction for better risk-reward

Time Horizon: 3-5 years minimum to realize full potential

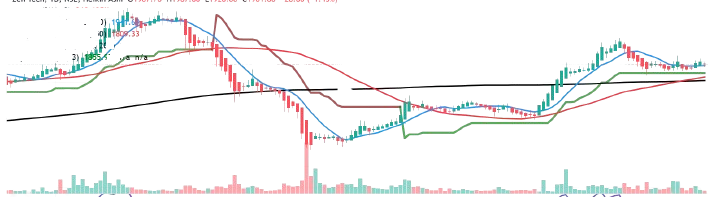

** Zen Tech on daily chart, expected to take support at 200-day SMA and 50-day SMA stationed at a very crucial position.

💡 CONCLUSION & FINAL THOUGHTS

While the company's market leadership, strong order book, and financial health provide a solid foundation, investors must navigate the challenges of premium valuations and execution volatility.

Investment Approach: Consider Zen Technologies as a core holding in a diversified defence technology portfolio, but time your entry carefully and maintain realistic expectations about short-term volatility.

📞 ANALYST CONTACT

This newsletter is prepared for informational purposes only and does not constitute investment advice. Please consult with qualified financial advisors before making investment decisions.

Disclaimer: All financial data and projections are based on publicly available information and company disclosures. Past performance does not guarantee future results. Investing in equity markets involves substantial risk of loss.

Let Us Talk

What are your views on Zen Technologies’ high valuations and profit volatility?

Can its order book and defence sector tailwinds justify the premium, or are there better opportunities in the sector? Share your thoughts below!

Zen Technologies are in the field where to be relevant the company must keep revising it's training materials one for relevance purposes and the technological advancements. A key requirement would be translating to other major languages and building a network of people and organizations using the company's training materials and organizing annual meets. I don't know, the company nay be doing it. These and such other services and initiatives puts the company in a powerful position with their customers and also adds competitive strength. Armies don't change vendors so easily.

You have not written anything on their cash flows !