About the Company

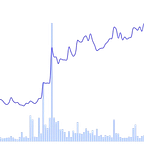

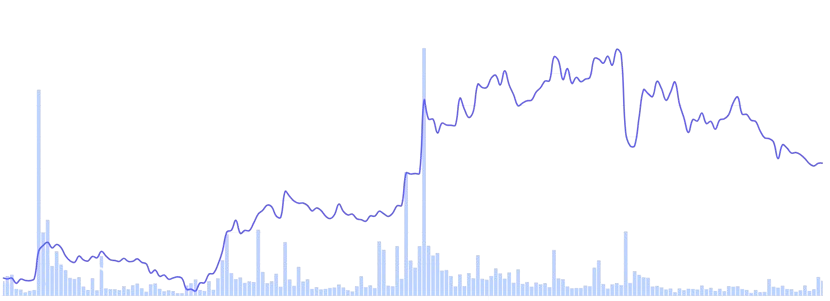

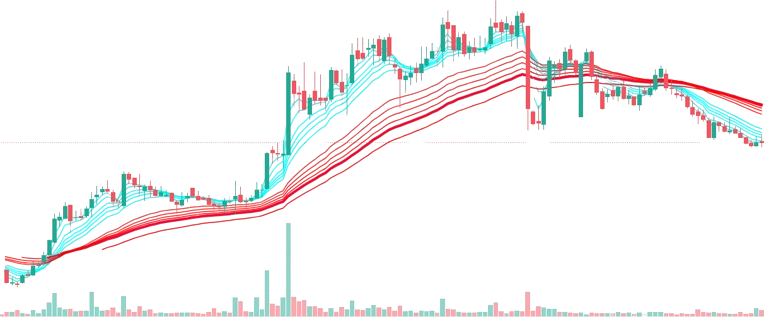

eMudhra Ltd. is India’s leading Digital Trust and cybersecurity solutions provider with operations across 25 plus countries. The company is rapidly transitioning from a domestic trust services leader to a global cybersecurity platform. Despite strong revenue growth and accelerated momentum in Q2 FY26, the stock trades near 52‑week lows due to sector weakness and short‑term margin pressures — creating a potential value opportunity.

CMP: ₹618 | Mcap: ₹5,100 Cr | TTM Revenue: ₹606 Cr | TTM Op Profit: ₹141 Cr

Business Overview

The company operates across two major segments: Digital Trust Services (23%), which includes digital signatures, SSL/TLS, IoT certificates, and PKI services, and Enterprise Solutions (77%), covering PKI, IAM, MFA, encryption, and the emSigner workflow digitization platform. It has a strong global footprint spanning India, the USA, Europe, the Middle East, and APAC. Strategic expansion has been driven by the acquisition of CRYPTAS in Europe and the proposed AI Cyberforge acquisition in North America.

Financial Performance Snapshot

Quarterly Trend (Q2 FY25 → Q2 FY26)

Revenue grew from ₹141 Cr → ₹173 Cr with margins stabilizing at 24%.

Q2 FY26 delivered 18% QoQ growth—its strongest sequential growth.

Annualized revenue run‑rate now stands at ₹650–700 Cr.

Yearly Trend (FY24 → FY25)

FY25 revenue grew 39% to ₹519 Cr; PAT up 13% to ₹87 Cr.

FY24 revenue had surged 50% to ₹373 Cr with strong Middle East traction.

Margins dipped from 29% (FY24) to 24% (FY25) due to global expansion and acquisitions.

Balance Sheet & Cash Flow

Virtually debt‑free with only ₹16 Cr borrowings.

Net worth > ₹800 Cr, strong reserves for future growth.

FY25 operating cash flow grew 40% to ₹102 Cr, excellent earnings quality.

Negative working capital cycle (-240 days) enhances cash efficiency.

Valuation Overview

The company currently trades at a P/E of 54x (Industry Average 32x), a premium that aligns with its strong structural growth story. This valuation premium is supported by its leadership position in digital trust and PKI, a robust global expansion pipeline, a high-visibility recurring revenue model, and strong industry tailwinds that continue to reinforce long-term growth.

Strategic Developments

Key Acquisitions

CRYPTAS (Europe): Entry into EU cybersecurity market; adds eIDAS‑qualified services.

AI Cyberforge (Planned): Strengthens North America presence in credential security.

Major Project Wins

Fortune 500 Managed PKI deal in USA.

UAE banking sector digital trust implementation.

Defence forces project in India.

Growth Drivers

Zero Trust adoption accelerating globally.

IoT expansion requiring device‑level PKI.

Post‑quantum cryptography transition (2025–2030).

India’s DPDP Act driving local cybersecurity demand.

Large untapped markets in EU & North America.

Risks & Challenges

Continued margin pressure from international expansion.

Integration risk of global acquisitions.

High competitive intensity from DigiCert, Entrust, GlobalSign.

Premium valuation leaves limited room for execution misses.

Currency fluctuations impacting profitability.

Investment View

The stock is currently down nearly 40% from its peak and is consolidating near a strong support zone, indicating a potential base-building phase. Fundamentally, eMudhra remains well-positioned with a solid global expansion strategy, strong revenue visibility, and healthy financials, supporting a favorable long-term outlook. The risk-reward profile also appears attractive and overall, the setup suits long-term investors who can comfortably withstand near-term volatility.

Conclusion

eMudhra is evolving from an India‑centric trust services provider into a global cybersecurity challenger with strong multiyear tailwinds. Despite temporary margin pressures, the company’s growth levers—Europe expansion, North America foray, Zero Trust, IoT security, digital workflows, and quantum‑safe PKI—position it for strong compounding.

With the stock near its 52‑week low and business fundamentals intact, the risk‑reward setup remains favorable for long‑term accumulation.

“Thehraw—when slowness becomes strength”

Disclaimer

This analysis is intended solely for educational and informational purposes and does not constitute any investment or financial advice. Past performance is not indicative of future results. All information is sourced from public company filings, analyst reports, and third-party sources believed to be reliable. In accordance with SEBI guidelines, market data is presented accordingly. Investors should conduct independent research, perform due diligence, and consult qualified financial advisors before making any investment decisions. The views expressed are personal and may be subject to errors or bias.