EXECUTIVE SUMMARY

Mamata Machinery Limited, currently trading at ₹420 with a ₹1,000 crore market cap, stands at a strategic inflection point driven by regulatory momentum, strong execution, and breakthrough innovation in cost-effective recyclable film technology. The company is debt-free with ₹71 crores cash (Sept 2025) and ranks among the top five global converting machinery makers.

INNOVATIONS & RECENT DEVELOPMENTS

Breakthrough: Recyclable High-Barrier Film

India consumes 1 million tons of non-recyclable PET-PE laminates annually. Mamata’s new solution provides:

High-barrier recyclable film at ₹250/kg (vs ₹320/kg alternatives)

Certified performance by Singapore labs & Indian Institute of Packaging

First-of-its-kind full ecosystem: extrusion + converting + packaging equipment

Market Potential: Even 10% conversion → 100,000 tons addressable

FINANCIAL PERFORMANCE

Q2/H1 FY26 Snapshot

Revenue: +25% (Q2), +31% (H1)

PAT: Soft Q2 due to higher exhibition spend (₹5.3o cr), but H1 +47%

Order Book: ₹144 crores; ₹134 cr execution expected in H2 FY26

VALUATION & COMPETITIVE POSITIONING

Valuation Metrics

CMP: ₹420

P/E: 24x (vs peer median 35x)

ROE: 27% (highest among peers): ROCE: 35%

STRATEGIC ROADMAP

Medium-Term (3–5 Years)

Revenue CAGR target: 18–20%

Become market leader in recyclable film solutions

Leverage 4,500+ installed base for cross-selling

Long-Term (5–10 Years)

Build India’s first packaging machinery conglomerate via M&A

Grow to global top-tier level in packaging machinery

RATING

Mamata Machinery offers a compelling mix of strong fundamentals, global presence, innovative recyclable film technology, and a healthy order book—yet the stock still trades at a discount to peers. While near-term volatility from tariffs and exhibition expenses may continue, the long-term structural outlook remains positive.

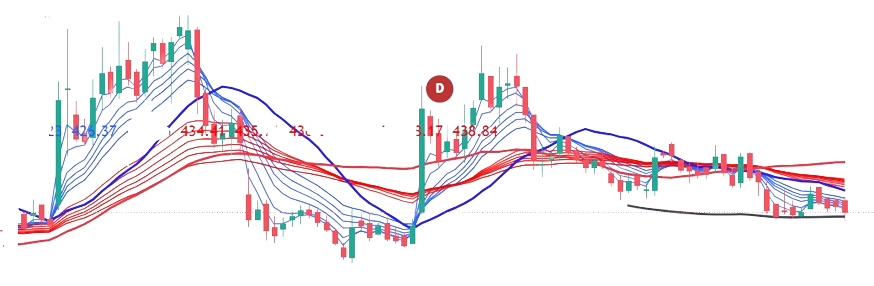

From a technical standpoint, the stock has corrected roughly 33 percent from recent highs and is currently testing its 200-day moving average—a level often associated with strong support.

It now sits inside the 62 percent Fibonacci retracement zone, a region where long-term reversals typically begin.

Meanwhile, the RSI around 43 and declining volumes suggest a phase of accumulation rather than selling pressure.

For traders, this offers an interesting setup:

Positions may be considered with disciplined stop-losses, aiming for 20 to 30 percent upside in the near term.

Key triggers to watch include:

Q3 FY26 results, and

Commercial announcements around Mamata’s recyclable film technology.

These events have the potential to significantly re-rate the stock.

Analyst’s View: Accumulate on dips, with a 6- to 18-month perspective.

Disclaimer

This analysis is intended solely for educational and informational purposes and does not constitute any investment or financial advice. Past performance is not indicative of future results. All information is sourced from public company filings, analyst reports, and third-party sources believed to be reliable. In accordance with SEBI guidelines, market data is presented with a three-month lag. Investors should conduct independent research, perform due diligence, and consult qualified financial advisors before making any investment decisions. The views expressed are personal and may be subject to errors or bias.