📋 Executive Summary

SEAMEC Limited is India’s leading offshore marine services provider with the largest fleet of Diving Support Vessels, Offshore Support Vessels, and bulk carriers across India and the Middle East. Incorporated in 1986, the company is at a critical inflection point—while technical charts indicate a breakout from consolidation, fundamentals remain mixed. Q1 FY26 results showed robust margin expansion despite modest revenue gains, supported by fleet expansion through strategic acquisitions that position SEAMEC for medium-term growth. However, operational headwinds such as vessel breakdowns and seasonal monsoon disruptions continue to drive earnings volatility.

📈 Financial Performance Analysis

Q1 FY26 Performance:

In Q1 FY26, SEAMEC Limited reported revenue of ₹231 crore, a modest 4% YoY growth, but delivered strong profitability with EBITDA rising 45% YoY to ₹117 crore and PAT surging 52% to ₹76 crore compared to ₹50 crore last year. Operating margins expanded significantly to 46% from 33% in FY25, supported by improved fleet utilization, which stood at a robust 93%.

FY 2024-25 Consolidated Performance:

SEAMEC Limited reported revenue of ₹652 crore, down 11% YoY from ₹729 crore, with EBITDA of ₹244 crore reflecting an operating margin of 33%. Net profit declined 27% YoY to ₹88 crore from ₹121 crore, while ROCE and ROE stood at 9% each, showing an improvement to 11% and 10% respectively in Q1 FY26.

🚢 Recent Developments

Positive Catalysts:

Fleet Expansion: Completed acquisition of "SEAMEC AGASTYA" (ex-NPP Nusantara) for US$23M, deployment expected December 2025

Contract Wins: Secured additional projects including PRP VIII and Daman Upside Development

Operational Challenges:

Vessel Breakdowns: SEAMEC Swordfish went off-hire in August 2025 due to technical issues

Seasonal Impact: Q2 FY26 expected to be subdued due to monsoon season

💪 Competitive Moat Analysis

Strengths:

Technical Expertise: 25+ years of specialized DSV operations and subsea services

Fleet Advantage: Largest multi-support vessel fleet in India/Middle East

Client Relationships: Strong ties with ONGC and major oil & gas players

Long-term Contracts: Most vessels secured on 3-4 year charters providing revenue visibility

Vulnerabilities:

Asset-Heavy Model: High capital intensity and maintenance requirements

Cyclical Exposure: Dependent on oil & gas capex cycles

Client Concentration: Heavy reliance on ONGC and Indian offshore market

🌍 Growth Drivers & Future Outlook

Industry Tailwinds:

Global offshore drilling market projected to grow from $36B (2023) to $80B+ by 2033 (8% CAGR)

India's Maritime Vision 2030 and 100% FDI in energy subsectors

Rising global oil demand projected at 103.9 million bpd in 2025

Company-Specific Catalysts:

Fleet Modernization: Phasing out older vessels (SEAMEC 1, 2, 3) for younger, more efficient assets

Geographic Expansion: Targeting Middle East markets (Saudi Arabia, UAE, Qatar)

Operational Leverage: Older vessels fully depreciated; breakeven at $30,000/day yields 25% returns

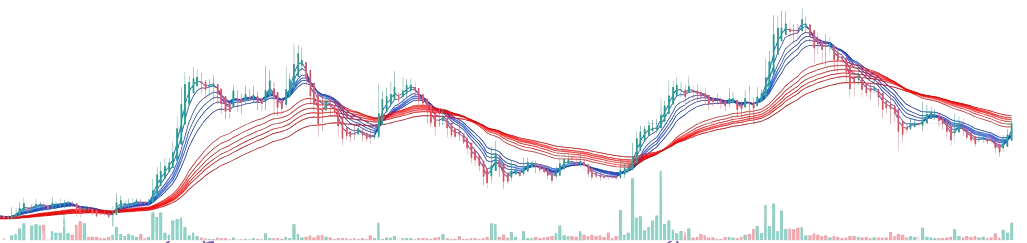

🎯 Valuation Analysis & Price Targets

Current Metrics (at ₹988): • P/E Ratio: ~22x (based on TTM earnings) • Market Cap/Revenue: 3.2x (₹2,064 Cr / ₹652 Cr) • EV/EBITDA: Reasonable given asset-heavy nature • Debt-to-Equity: Conservative 0.21x

Technical Price Targets:

For short-term traders looking at one to three months, we see resistance at 1,050 to 1,100 rupees - that's 6 to 11% upside potential, with support at 940 to 950 rupees.

Medium-term investors, looking at three to twelve months, should focus on our primary target - representing 20 to 30% upside. A technical breakout could drive prices further, offering 50% upside approximately.

For long-term investors with a twelve-month-plus horizon, our extended targets may reach - that's 65 to 75% upside potential.

Key levels to watch: support at 940 to 950 rupees, breakout above 1,145 rupees, and a stop-loss at 945 rupees for risk management.

Investment Strategy:

Aggressive Investors: Can consider current levels with strict stop-loss

Conservative Investors: Wait for pullback to ₹950-960 range

Long-term Investors: Accumulate on any weakness below ₹950

🎯 Bottom Line

SEAMEC Limited presents a compelling turnaround story with technical charts supporting fundamental recovery. The company's strategic positioning in India's offshore services market, fleet modernization efforts, and improving financial metrics create a positive medium-term outlook. While operational challenges persist, the stock appears well-positioned for a re-rating cycle.

Disclaimer

This analysis is for educational and informational purposes only and does not constitute financial advice. All data is sourced from public company filings, analyst reports, and third-party sources believed to be reliable. In line with SEBI’s guidelines, all market data is presented with a three-month lag. Investors should carry out their own due diligence and consult the financial advisor before making any investment decisions. The views expressed are personal and may be subject to errors or bias.