COMPANY OVERVIEW

Sharda Cropchem is an asset-light, IP-driven agrochemical exporter operating across 80 plus countries, with a strong presence in Europe, NAFTA, LATAM, and other global markets. Its business is primarily driven by agrochemicals (86%)—including herbicides, insecticides, fungicides, and biocides—while the non-agro segment (14%) covers conveyor belts, dyes, and V-belts. The company follows a fully outsourced manufacturing model, allowing it to scale efficiently.

With a market cap of around ₹7,700 crore, promoter holding of 74.80%, and ₹794 crore in cash with zero debt, Sharda maintains a financially strong and strategically flexible position.

FINANCIAL PERFORMANCE: STRONG RECOVERY

Q2 FY26

Revenue: ₹929 Cr (↑20% YoY)

EBITDA: ₹138.9 Cr (↑71% YoY), 15% margin

FY 2024 - 25

Sharda Cropchem delivered a strong performance with ₹4,320 crore in revenue (↑37% YoY) and a sharp jump in net profit to ₹304 crore from ₹32 crore, supported by a healthy ROCE of 21.60% and ROE of 17.50%.

The improvement was driven by raw material normalization, pricing stability, and a strong recovery in its key European market.

GROWTH DRIVERS

Massive Registration Moat: With 2,994 active approvals, 1,068 pending registrations, and ₹450–500 crore FY26 capex dedicated to filings, Sharda Cropchem has a strong regulatory pipeline that ensures multi-year revenue visibility through new product-market launches.

Global Agrochemical Upcycle: The industry is recovering as inventory destocking nears completion, pricing and raw material costs stabilize, and demand shifts toward cost-efficient generics.

Margin Expansion: The company targets 15–18% EBITDA margins, supported by improving operating leverage and its fixed-cost-light model.

Management Guidance (FY26): Leadership expects 15% plus revenue growth, led by a continued focus on Europe and the expansion of high-value product registrations.

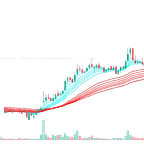

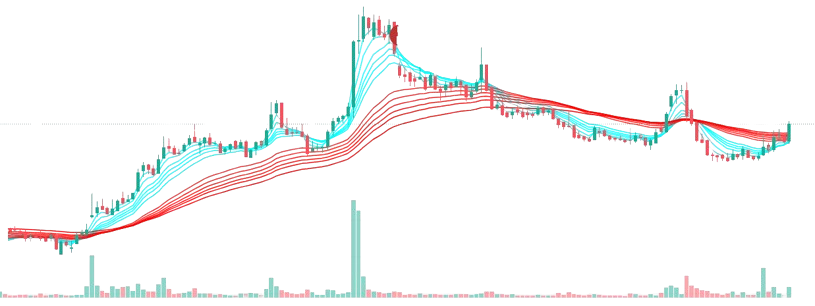

TECHNICAL ANALYSIS: BULLISH CONSOLIDATION

Sharda Cropchem is trading at ₹862, consolidating firmly within the ₹810–880 zone after its August 2025 peak of ₹1,181. The stock has established strong support at ₹810–820 and faces initial resistance at ₹900–920, with a more significant barrier at ₹1,000–1,050. Its structure of higher highs and higher lows reflects a well-maintained long-term uptrend and healthy underlying momentum.

Bottom Line: At the current level, the stock sits at an important inflection point. Sharda has moved above key moving averages and is attempting to shift into a renewed uptrend. A decisive close above ₹900 could trigger a strong bullish continuation, while an inability to hold above ₹830 may extend the consolidation phase.

KEY RISKS

Key risks for Sharda Cropchem include margin pressure from Chinese competitors and a heavy dependence on Europe, which increases regional exposure.

The company also faces high debtor days of 165, impacting working capital, and experiences seasonal weakness in Q3, which typically results in softer performance.

INVESTMENT POSITIVES

Sharda Cropchem enjoys a strong financial and competitive position, supported by a debt-free balance sheet with ₹794 crore in cash and a high promoter holding of 75%. The company operates in heavily regulated markets that create high entry barriers, helping protect its market share. Its margins have improved from 10% to over 15%, and with 1,068 pending registrations, it has clear long-term growth visibility.

CONCLUSION

Sharda Cropchem is emerging strongly from an industry downcycle, supported by improving margins, robust registrations, and strong European demand. With attractive valuations (15.5x vs justified 18–20x) and technical stability, the stock offers a REASONABLE UPSIDE over 12–18 months.

Suitable for investors with:

12–18 month horizon

Moderate risk appetite

Interest in asset-light global agrochemical exporters

DISCLAIMER

This report is for educational purposes only. Past performance is not indicative of future results. Investors should perform their own due diligence and consult a qualified financial advisor. Equity investments, especially in small-caps, carry significant risks including capital loss.