PNB Housing Finance Ltd is India's prominent housing finance company, promoted by Punjab National Bank since 1988. Operating through 189+ branches nationwide, the company focuses on retail lending with 98% of its loan portfolio in individual home loans, loans against property, and commercial space financing.

Key Metrics (Current):

Market Cap: ₹20,500 Crores

Current Price: ~₹780-790 (Post-CEO exit correction)

Book Value: ₹648 per share

P/E Ratio: 10x (Attractive vs sector average 15-20x)

🚀 Major Positive Factors & Trends

1. Exceptional Financial Performance

FY25 Revenue Growth: ₹7,685 crores (+9% YoY)

Net Profit Surge: ₹1,936 crores (+28% YoY)

Q1 FY26 Momentum: 23% YoY profit growth to ₹534 crores

EPS Growth: ₹74.49 in FY25 vs ₹58.81 previously

2. Affordable Housing Segment Explosion

143% YoY Growth in affordable housing loans (Q1 FY26)

Government Policy Tailwinds: PM Awas Yojana and housing-for-all initiatives

3. Asset Quality Renaissance

GNPA Improvement: Down to 1.06% (industry-leading levels)

Corporate NPAs: Reduced to just ₹68 crores

Clean Balance Sheet: Post-legacy NPA resolution

4. Robust Loan Book Expansion

18% YoY Growth in retail loans to ₹76,923 crores

₹1 Trillion Target: Retail assets by FY27

💰 Compelling Valuation Proposition

Undervaluation Evidence

P/E Multiple: 10x vs sector average 15-20x (50% discount)

P/B Ratio: 1.2x vs historical 1.5-2x sector range

Fair Value Models:

Peter Lynch Model: 150% upside potential

DCF/Relative Valuation: 108% upside

Analyst Targets: UBS target ₹1,300 (67% upside)

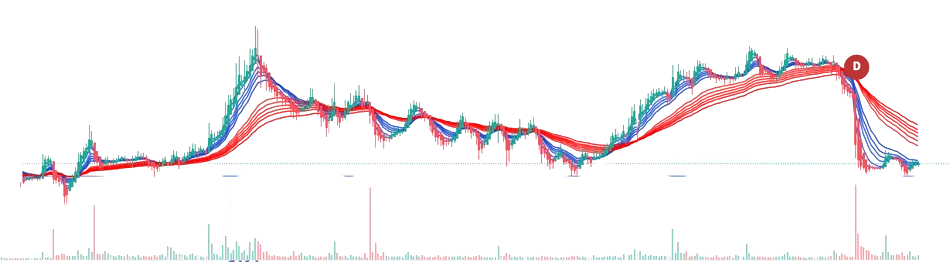

📈 Technical Recovery Signals

Oversold Conditions: RSI at 34 (attractive entry zone)

Support Levels: Strong support at ₹755-766 zone

Volume Spike: High-volume correction suggests capitulation

🎯 Investment Thesis

Why Now is Attractive

Temporary Discount: CEO exit created sentiment-driven selloff

Fundamental Strength: Underlying business momentum intact

Sector Leadership: Well-positioned for India's housing boom

Valuation Floor: Trading below intrinsic value estimates

Recovery Play: New leadership could unlock further value

🌟 Key Investment Highlights

✅ 28% Net Profit Growth in FY25

✅ 143% Affordable Housing Surge in Q1 FY26

✅ 1.06% GNPA - Industry-leading asset quality

✅ 50% Valuation Discount vs sector peers

⚡ Conclusion: The Turnaround Story

PNB Housing Finance represents a compelling turnaround opportunity disguised as a leadership crisis. The company's fundamentals remain robust with exceptional growth in high-margin affordable housing, improving asset quality, and attractive valuations.

The CEO exit, while creating near-term uncertainty, has provided an excellent entry point for long-term investors. With strong parentage, sector tailwinds, and a clear growth strategy, PNBHF is positioned to deliver significant returns as leadership stabilizes and execution continues.

Investment Rating: BUY on dips

Risk-Reward: Attractive (3:1 upside-to-downside ratio)

Disclaimer: This analysis is for informational purposes only. Please consult with qualified financial advisors and conduct your own due diligence before making investment decisions. Past performance does not guarantee future results.

Let's Talk!

What are your thoughts on PNB Housing Finance's current situation? Do you see any hidden opportunities we might have missed, or do you share our concerns about the company's structural challenges?