Founded in 1996 and headquartered in Ahmedabad, Astral Ltd is a leading force in India’s building materials sector. With 19 manufacturing units across India, the UK, and the USA, and a distribution network of over 229,000 dealers and 3,303 distributors, the company offers products ranging from CPVC and PVC pipes and adhesives to sanitaryware, faucets, tanks, and paints. It is listed on the NSE and BSE and had a market cap of ₹38,700 crore.

📊 Financial Performance: Mixed Signals in FY25

Q1 FY25

Revenue: ₹1,384 crore (+8% YoY)

Net Profit: ₹120 crore (+47% YoY)

Branding expenses: ₹20 crore (one-time cost)

Q2 FY25

Revenue: ₹1,370 crore (+0.5% YoY)

Net Profit: ₹109 crore

Hit by 13% fall in PVC prices and ₹10–15 crore inventory loss

Q3 FY25

Revenue: ₹1,397 crore (+2% YoY)

Net Profit: ₹113 crore (–29.8% YoY)

Despite stable revenue and margin control, profits were hit by cost pressures and weak volume growth

🏭 Expansion & Strategic Updates

Capex: ₹282 crore (H1 FY25); full year estimate ₹350 crore

New Plants:

Hyderabad: 21,000 MT pipes + tanks production started

Ghiloth: CPVC and SWR fittings operational

Kanpur: Construction underway, trials by Q4 FY25

Product Launches:

Fire Pro UL-certified fittings for exports (Europe, Gulf)

Channel drains and new valve/fitting lines in the pipeline

OPVC pipes ready pending BIS approval

Export Market: Dubai office opened to capture UAE, Gulf, and African demand

📈 Historical Financials: Consistency Meets Caution

FY23

Revenue: ₹5,158 crore

EBITDA Margin: 15.60%

CFO: ₹557 crore; FCF: ₹77 crore (hit by ₹480 crore in capex)

ROCE: 18.70%

FY24

Revenue: ₹5,642 crore

EBITDA Margin: 16%

CFO: ₹825 crore; FCF: ₹610 crore

ROCE: 23%

FY25

Revenue: ₹5,832 crore

EBITDA Margin: 16%

CFO: ₹630 crore; FCF: ₹514 crore

ROCE: 20.30%

Key Trends:

Revenue grew at a CAGR of 19.70% from FY20 onwards

Cash generation strengthened post-capex cycle

ROCE remains strong, though slightly below key peer

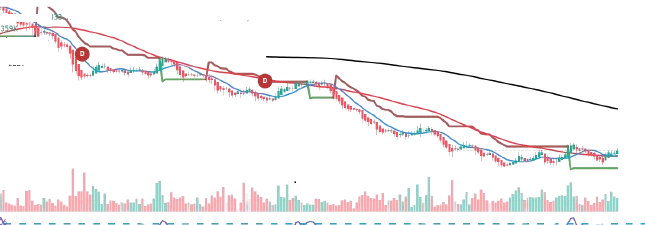

📉 Valuation & Technicals: Is the Premium Justified?

P/E: 74 against the industry median of 26

Stock Price down almost 40% from 52-week high of ₹2,454 and RSI standing neutral at 62

Shareholding Trends (March 2025):

FIIs: 20.17%; DIIs: 14.60%; Promoters: 54.10% (stable) and Public: 11.12%

🧮 SWOT Analysis

Strengths

Brand dominance in CPVC market; Vast distribution and manufacturing scale and Low leverage (Debt to Equity 0.03)

Weaknesses

High valuations; Underperformance in new business verticals; Thin free cash flows during heavy capex cycles

Opportunities

Infrastructure tailwinds like Jal Jeevan Mission; Adhesives & paints growing at 15% CAGR and Export potential (Africa, Gulf, Europe)

Threats

Raw material and FX volatility; Competitive pressure from Finolex, Supreme and Regulatory risks in plastic usage

Price Action on Daily Chart: New entrants might consider accumulating for a better risk-reward profile as it is on the Golden Crossover at 10 – 50 days SMA and SuperTrend is suggesting the up move and volumes are surging up.

🔮 The Road Ahead

Revenue CAGR guidance: 15–20% (FY24–FY26)

New product lines to contribute ₹1,500 crore over 5 years

Adhesive market share goal: 6–7% from 4.70% currently

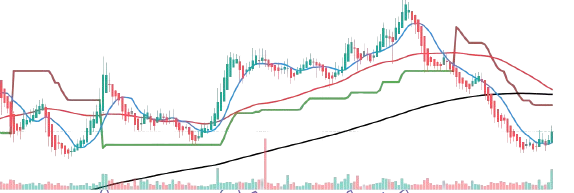

📌 Weekly Chart and the Final Take

Astral stands at a turning point — a fundamentally sound company entering a diversification phase. While its core remains strong, the performance of newer segments and high valuation metrics warrant caution.

From the weekly chart, seems the stock has taken the support from the lows of March 2023 and Jun 2022, and the stock seems ready for an up move and may be an opportunity with a focus on execution in FY26.

🛑 Disclaimer

This analysis is for educational and informational purposes only and does not constitute any financial advice. All data is sourced from public company filings, analyst reports, and third-party sources believed to be reliable. In line with SEBI’s guidelines, all market data is presented with a three-month lag. Investors should carry out their own due diligence and consult the financial advisor before making any investment decisions. The views expressed are personal and may be subject to errors or bias.

💬 Let Us Talk!

📣 What's your view on Astral's diversification strategy?

📊 Are the valuations too steep or just right for a long-term play?

👇 Drop your comments below!

👍 Like this report?

🔔 Subscribe for more deep-dive research like this!