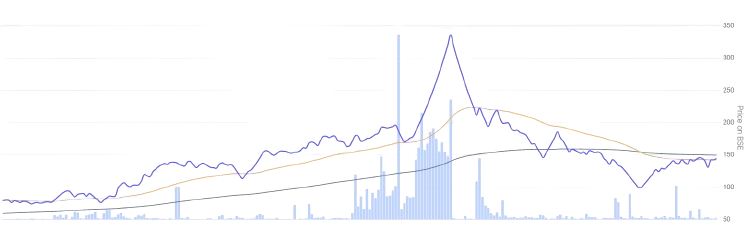

Systematix Corporate Services has surged an impressive 78.56% over the past year. As a SEBI-registered Category I Merchant Banker, it operates in merchant banking, financing, and transactional services. But amid rising volatility and inconsistent earnings, can this momentum hold? With an updated current ratio of 2.35, let’s break down whether the rally is built on solid ground—or hype.

Company Snapshot: What Does Systematix Do?

Systematix operates via three core verticals:

Merchant Banking: Advises on IPOs, rights issues, debt placements, valuations, and ESOPs.

Financing: Provides loans against shares and margin funding through its NBFC arm.

Transactional Services: Offers broking, wealth management, portfolio services, and distributes mutual funds and insurance.

Its asset-light structure allows scalability but increases exposure to capital market cycles.

Financial Overview: Strength in Numbers?

As of March 31, 2024 (consolidated):

Market Cap: ₹1,970 Cr – firmly in small-cap territory.

P/E Ratio: 30.00 – elevated, yet well below its peers.

ROCE / ROE: 48.40% / 42.40% – stellar performance with a 5-year average of 20% and 14.59% respectively.

Debt-to-Equity: 0.17 – nearly debt-free.

Current Ratio: 2.35 – excellent liquidity.

Promoter Holding: 70.60% – stable, though down from 74.23%.

FII Holding: 3.57%; DII: 0.04% – muted institutional interest.

10-year CAGR: 59% – exceptional long-term growth.

Bottom Line: Systematix is financially sound, but its rich valuation and weak institutional backing raise red flags.

Recent Developments: Growth or Growing Pains?

Key updates:

Stock Split (Nov 2024): A 10:1 split to improve liquidity.

Capital Raise: ₹103.12 Cr at ₹1,531/share, before split, to fund expansion.

Revenue Surge: Q2 FY25 standalone revenue jumped 3056.03% YoY, but consolidated sales declined.

Caution: While moves like fundraising and rebranding indicate ambition, falling consolidated revenue points to structural cracks.

Financial Performance: A Mixed Bag

FY 2023–24 (Consolidated)

Revenue: ₹145.97 Cr (+101.26% YoY), Net Profit: ₹53.35 Cr (+950.20% YoY) and EPS: ₹4.11

Highlights: Robust growth in merchant banking and financing; better working capital efficiency boosted cash flows.

Q1 FY 2024–25

Revenue: ₹30.50 Cr (+50.2% YoY), Net Profit: ₹1.74 Cr (–60.7% YoY)

· Profit fell despite revenue growth—likely hit by higher costs.

Q2 FY 2024–25

Revenue: ₹43.82 Cr (–8.75% YoY), Net Profit: ₹18.58 Cr (–22.36% YoY)

Margin contraction to 37.78% hints at lower advisory income.

Conclusion: FY24 was a breakout year, but FY25's rocky start suggests instability beneath the surface.

Competitive Position: Is the Moat Wide Enough?: Systematix’s edge lies in:

SEBI License: High regulatory entry barriers, Asset-Light Model: Scalable with high asset turnover (12.63), Diversified Clients: Broad mix from FIIs to retail investors and Cash Efficiency: Converts 120.55% of operating earnings into cash.

But:

Brand Weakness: Lacks visibility vs. peers like JM Financial, Cyclicality: Heavily reliant on volatile fee-based income and Scale: Small size limits institutional appeal.

SWOT Summary

Strengths:

Exceptional ROCE/ROE, Low leverage and Strong liquidity and cash flow metrics

Weaknesses:

Profit volatility and Rising employee expenses (31.89% of revenue)

Opportunities:

IPO boom, Wealth management demand and Digital platform scaling

Threats:

Bigger competitors, Regulatory changes and Market turbulence

Valuation Check: Pricey or justified?

P/E: 30.00 – high for a small-cap; peers like PTC India Financial trade at 15

Fair Value Range (P/E 15–20): ₹123–164 based on FY24 EPS of ₹4.11

EV/EBITDA: 38.33 – rich by industry standards

Verdict: Premium valuation backed by strong returns—but sustained earnings are crucial for justification

What’s Next? Outlook & Red Flags

Growth Catalysts:

Expanding IPO ecosystem, HNI and wealth management uptick and Recent capital infusion for scaling tech and financing

Risks:

Unpredictable earnings, Falling promoter stake and Broader market/regulatory pressures

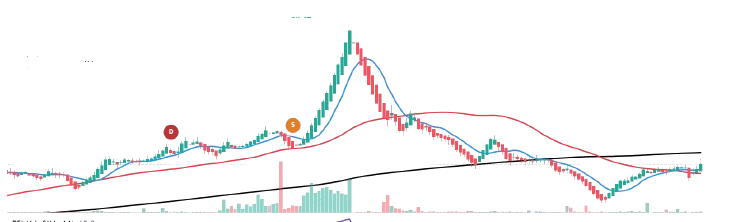

Technical View: Short-term uptrend capped; weak momentum after a 6-month 18.14% slide

Final Word: Hold, But Watch Closely

Systematix scores big on fundamentals—high ROCE, strong ROE, near-zero debt, and liquidity. Yet, profit dips, rich valuation, and tepid institutional interest urge restraint.

Hold with caution. Existing investors may Hold with caution. New entrants? Wait for breakouts and time the entry.

Like what you read? Subscribe for exclusive insights on under-the-radar stocks and smart investing strategies. Join us on Substack.

Disclaimer: This analysis is for educational and informational purposes only and does not constitute any financial advice. In its latest circular, SEBI has clarified that individuals providing stock market education must use stock price data with a three-month lag. Accordingly, all data and charts presented here comply with these guidelines. Investors should conduct their own due diligence before making any investment decisions. The opinions expressed are personal, potentially biased, and may contain inaccuracies. Additionally, all figures are subject to verification.

💬 Let’s Talk

Do these hidden performers fit into your portfolio strategy? Want help building a screener tailored to your style?

📧 Reply here or drop us a message—we're always up for a thoughtful investing conversation.