Windlas Biotech has been a rising name in India’s pharmaceutical industry, but recent financial trends and operational concerns raise questions about its future. Is Windlas a strong long-term bet, or is its growth story at risk? Let's dive into the details.

Company Overview

Windlas Biotech, specializes in generic formulations and operates as a Contract Development and Manufacturing Organization. Established in 2001, the company has four manufacturing facilities in Dehradun, serving both domestic and international markets.

Core Business Segments

CDMO Services – Partnering with pharma companies to develop and manufacture formulations.

Domestic Generics – Selling its own branded generic medicines.

Exports – Expanding into regulated markets, including the United States.

Despite its diversified model, Windlas faces stiff competition from larger pharmaceutical giants with stronger API capabilities.

Competitive Edge & Challenges

Strengths

Top-5 CDMO Status – A trusted partner for major pharmaceutical firms.

Proprietary Technology – Differentiated formulations and production efficiencies.

Pan-India Distribution – A strong domestic network.

Weaknesses

Thin Margins – Profits lag behind industry leaders.

Export Scale – Limited presence in highly regulated markets.

Client Concentration Risk – Dependence on a few key CDMO partners.

Recent Developments

📈 Q2 FY25 Growth – Revenue surged 22% YoY, outpacing the market.

💊 New Product Launches – Expanding chronic therapy generics.

🏭 Facility Upgrades – Investments in Dehradun to increase capacity.

🌎 Export Expansion – Progress in US regulatory approvals.

However, cost pressures and operational inefficiencies raise concerns about sustainability.

Financial Overview

FY 2022-23

Ø Revenue: ₹523 Cr (+10.12% YoY)

Ø Net Profit: ₹42 Cr

Ø EBITDA Margin: ~12%

FY 2023-24

Ø Revenue: ₹644 Cr (+23.21% YoY)

Ø Net Profit: ₹56 Cr

Ø EBITDA Margin: ~13%

Q1 & Q2 FY 2024-25

Ø Q1 Revenue: ₹170 Cr (+18% YoY)

Ø Q2 Revenue: ₹195 Cr (+22% YoY)

Ø Net Profit: ₹15 Cr (Q1), ₹18 Cr (Q2)

Ø EBITDA Margin: 13-14% (Stable)

Despite strong topline growth, margin improvements remain limited, raising questions about profitability.

Future Growth Projections

Ø Company Guidance: ₹1,000 Cr revenue by FY27, 15% EBITDA margin.

Ø Analyst Forecasts: More conservative at ₹900 Cr, citing export and competition risks.

While growth expectations are optimistic, execution remains a key challenge.

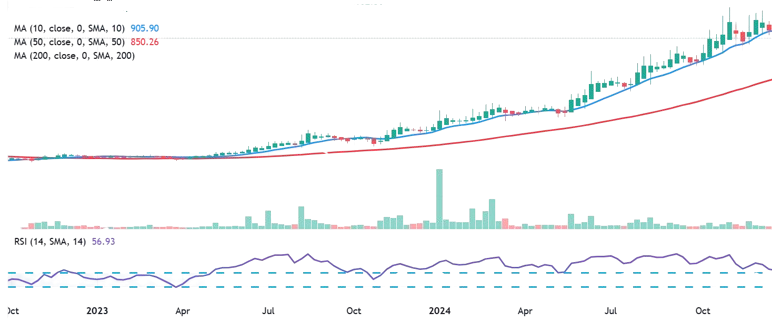

Chart, Valuation & Investment View

Ø P/E Ratio: 35.40x (Industry avg: 36.73x and on the lowest band to its peers)

Ø ROE: 14%

Ø ROCE: 18%

Ø Debt-to-Equity: 0.04x (Healthy balance sheet)

At 35x P/E, Windlas appears fairly valued, but given its margin constraints and competition, Accumulation on dips for long-term growth may be the mantra for investors.

Risks & Concerns

Competition – Larger API players could squeeze margins.

Raw Material Costs – Unpredictable price hikes threaten profitability.

Regulatory Risks – Delays in US approvals could slow growth.

Client Concentration – Over-reliance on a few CDMO partners.

Final Thoughts

Windlas Biotech has showcased strong growth and financials, supported by strategic expansion. However, valuation concerns and market risks persist. Investors should weigh strong fundamentals against regulatory and competitive challenges.

📌 Recommendation:

At 35x P/E, Windlas appears fairly valued, but given its margin constraints and competition, Accumulation on dips for long-term growth may be the mantra for investors. The investors may seek to hold for long term gains.

Disclaimer: This analysis is for educational and informational purposes only and does not constitute any financial advice. In its latest circular, SEBI has clarified that individuals providing stock market education must use stock price data with a three-month lag. Accordingly, all data and charts presented here comply with these guidelines. Investors should conduct their own due diligence before making any investment decisions. The opinions expressed are personal, potentially biased, and may contain inaccuracies. Additionally, all figures are subject to verification.

What’s Your Take?

Do you believe Windlas can sustain its growth, or do valuation concerns make you skeptical? Share your thoughts in the comments below!